$Atlassian(TEAM)$

要深入研究美股公司,财报季是最好的机会。每个财报季的来临总是让人感到有些疲惫但是又兴奋不已。因为时差的关系,可能需要凌晨四点起床看报告拆数据,听电话会议,但是每次财报季如果能发现一到两只牛股,又让人觉得一切付出都很值得。

TEAM是一个听说许久,但是一直还没覆盖的SaaS公司,他的Jira是很多互联网公司IT朋友很喜欢的一个产品。

TEAM财报初步评估 :

(1)收入比较大可能超预期,预计在30%~35%之间,因为调价的幅度比较大,而且 大部分前置Q1实现

(2)因为转云,FCF可能要有所牺牲,不确定

(3)目前 300亿不到的市值,对应FY20年管理层指引15.56亿 ,19.28倍PS。如果财报 增速 略 高于 管理层指引,落在30%以下区间,那么当前的估值就有较大的下行空间。

当然从历史来看 ,或者从产品,竞争优势,长期发展来看,Team是家值得关注的好公司,只是当下的价格,从投资角度来说可能没有很大的安全边际。

TEAM财报的核心要素

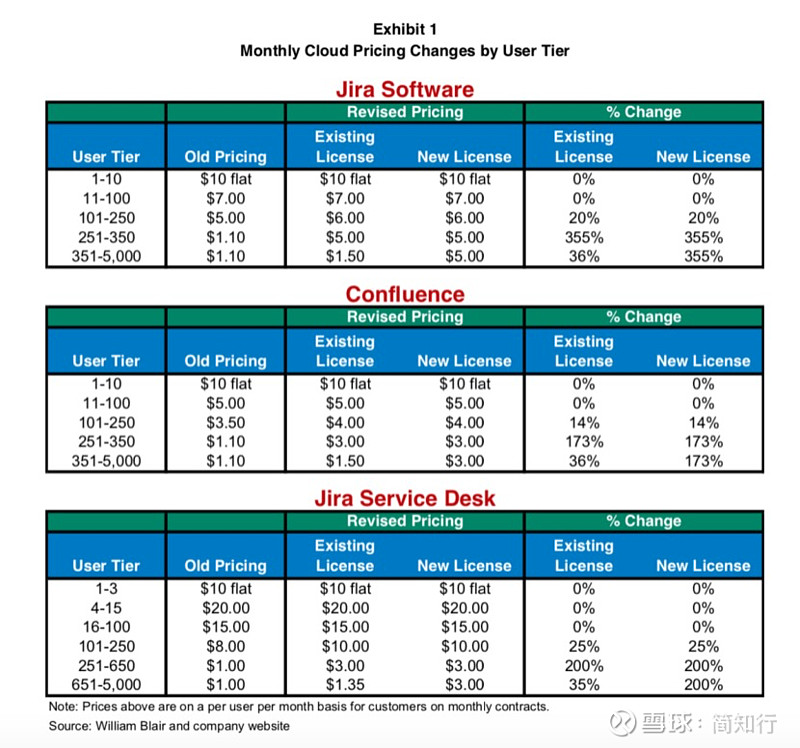

1. 提价的影响

(1)2019.9.1提价

(2)历史提价复盘&比较

TEAM近三年每年9月都会提一次价,而前两次提价财报一次大涨24%,一次大跌14%,那么本次提价对财报的影响也至关重要,也是财报预判的最关键要素

(3)本次提价分析及对财务影响

参照2018年的价格上涨的影响,高盛对财务的影响做了测算如下:

如果我们将由于20财年价格上涨而对当前GS估计的潜在收益进行分析,则20财年第一季度的递延收入总额为5.12亿美元(同比增长41%),收入为3.63亿美元。 (同比增长36%)vs。市场共识为4.98亿美元(同比增长37%)和3.52亿美元(同比增长32%)。 在20财年,此分析估计总递延收入为6.37亿美元(同比增长36%)和收入为16.08亿美元(同比增长33%),而市场共识分别为6.13亿美元(同比增长31%)和15.54亿美元(同比增长28%)。 在账单基础上,此分析导致20财年第1季度账单同比增长+ 41%,而市场共识为+ 33%和20财年,这导致账单同比增长+ 33%,而市场普遍预期为+ 28%增长。 19财年同比增长52%。

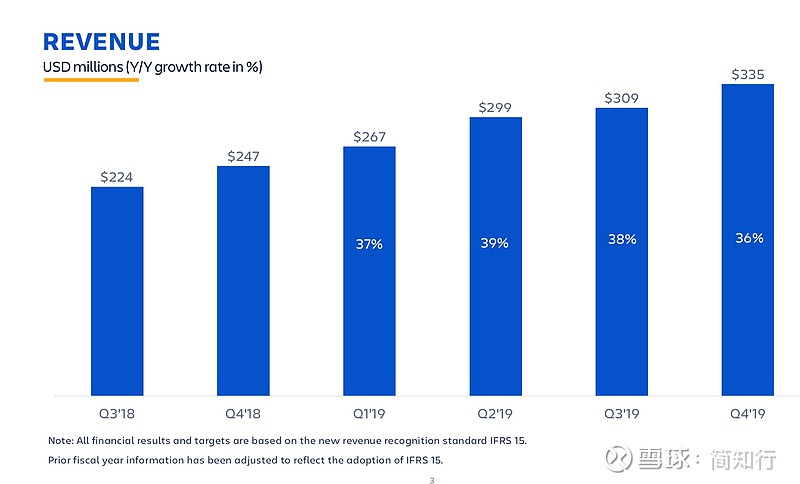

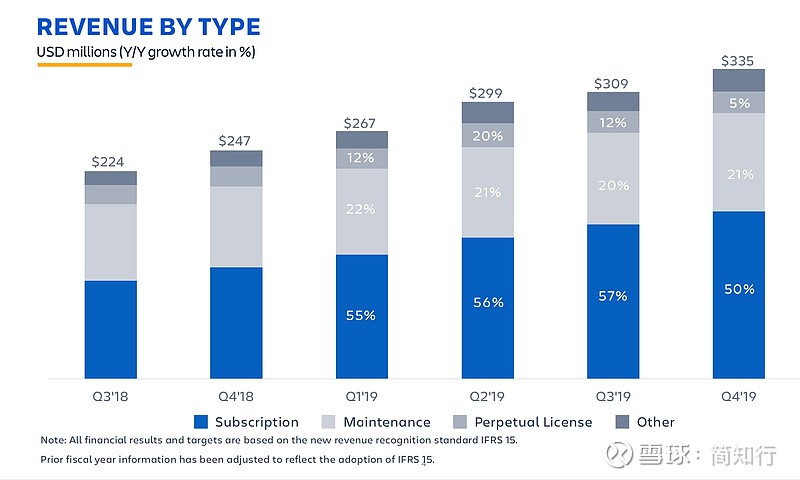

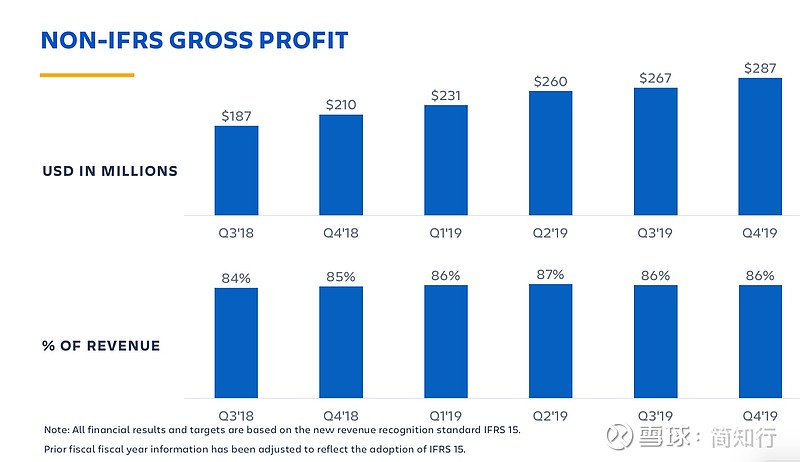

2. 关键业务数据

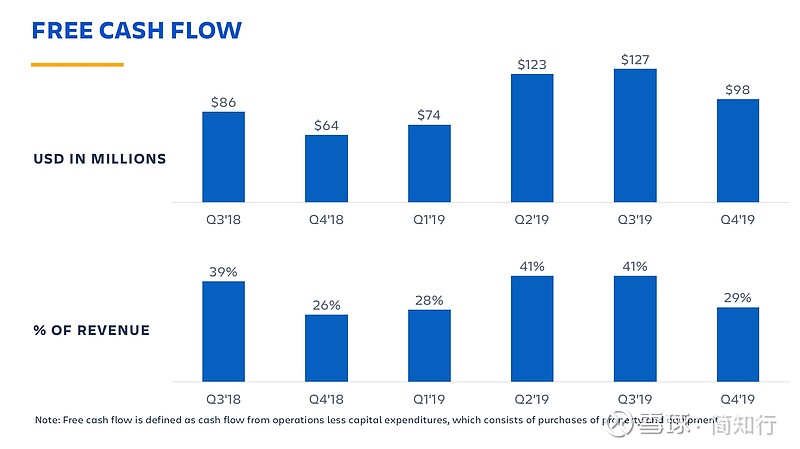

总结:在1B+以上体量保持高30%增长,实属不易 ,高毛利率(86%),30%-40%的自由现金流,难得的是连提三年价格之后,价格对比竞争对手还有很大优势,敢于提价也说明其竞争地位和产品粘性。当然最后还是数据说话,接下来几个季度的数据 应该可以客观反应提价和转云的变化。

3. 财报前盈利预测&估值

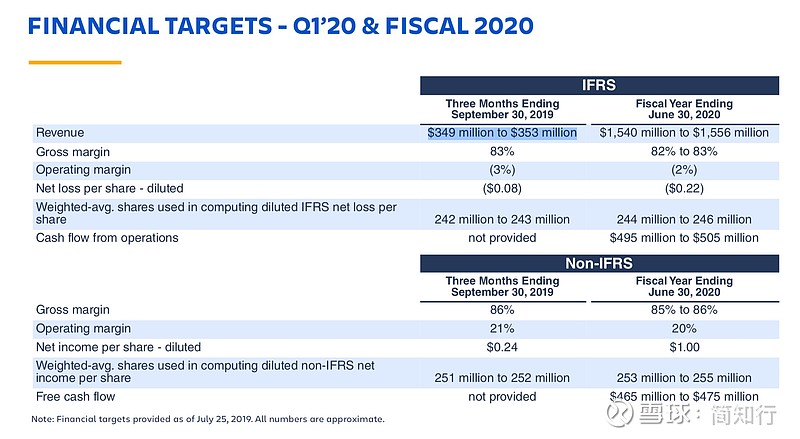

FY1Q20 管理层指引营收$349 million to $353 million ,FY20 15.4~15.56亿营收,yoy 28%. 当前估值截止 2019.10.16收盘市值301.9亿,对应FY20 约为19.5亿PS。

The consensus EPS Estimate is $0.24 (+20.0% Y/Y) and the consensus Revenue Estimate is $351.79M (+31.6% Y/Y). The consensus Revenue Estimate is 1.56B(+28.9% Y/Y))

初步评估:FY20Q1在涨价预期下,如果更新的全年指引增速低于30%,现有估值大概率无法支撑。

Note:管理层给予低预期的原因在于FY20是关键的云转型年 ,同时存在现金税和预付款影响,现金流也会受到影响,FY4Q的现金流就miss了。

20财年FCF指导为465-4.75亿美元,远低于cons的5.7亿美元。 FCF前景意味着11%的增长(2016财年为50%)和FCF利润率为30%(19财年为34%)。 FCF指南的不足反映出现金税增加了3,000万美元(公司在19财年获得了700万美元的税收优惠),以及前期许可交易减少带来的影响,因为收入组合更多地转向订阅。

全部讨论

Atlassian的总裁Jay Simons、首席营销官Robert Chatwani以及全新的投资者关系副总裁Matt Sonefeldt最近参加了JMP举办的Software Bus Tour。Matt 曾在私人控股的Gusto(JMP百强企业)和LinkedIn上任职。

会议中有一个要点值得关注:Atlassian的首席营销官在eBay任职了12年,为公司带来了新的见解,他在其中应用了从消费者电子商务到Atlassian的许多原则,其中包括:a)对“新商品的行为特征有深刻的了解”和现有客户”; b)建立顾客喜爱的品牌; c)以与电子商务公司使用商品推销方式相同的方式考虑客户扩展; (4)在云中运行的客户越多,Atlassian使用这些类型的原则的机会就越大; 5)10月份的价格上涨动态符合预期,该公司认为,即使在较高的价格点,它也提供了“巨大的交易”。

如果这种跨界的思维在2B领域可行,那么可以想象Atlassian的用户扩张也许会给投资者带来惊喜。毕竟在如此大的体量下,公司的增长依旧保持在30%的水平,多次提价也不影响客户粘性,令人惊叹

Atlassian Falls After Q1 Earnings Beat, Code Barrel Acquisition

Benzinga 10-18 04:14

Atlassian Corporation PLC(NASDAQ: TEAM) shares are falling after issuing weak 2020 earnings guidance.

First-quarter adjusted earnings came in at 28 cents per share, beating estimates by 4 cents. Sales came in at $363.4 million, beating estimates by $11.6 million.

The company issued strong second-quarter earnings and sales guidance, but 2020 earnings guidance was short of consensus estimates.

"We're out of the blocks in good form in fiscal 2020," said Mike Cannon-Brookes, Atlassian's co-founder and co-CEO. "We updated Atlassian's Cloud platform in a big way with new Free and Premium editions. Our disruptive model continues to win new customers, both large and small, and these new editions offer them more choice and capabilities."

Atlassian also announced the acquisition of Code Barrel.

"We are also excited to announce that Atlassian has acquired Code Barrel, the creator of Automation for Jira," said Scott Farquhar, Atlassian's co-founder and co-CEO. "Automation for Jira is already used by thousands of organizations to help them reduce repetitive work and unleash the potential of their teams. This acquisition is an important step as we continue to enhance our cloud products."Q1 Highlights:

Revenues were up 36% year-over-yearQuarterly cash flow from operations was $76.2 million7,060 net new customers were added

Atlassian shares traded down 3% in after-hours trading. The stock closed at $122.48 per share.

财报基本符合之前判断

FY1Q20 营收3.63亿,yoy36%,超出3.49亿~3.53亿指引,FY20指引15.6亿~15.7亿,yoy28.9%,EPS0.28超出 0.24的预期

1Q20 FCF$76M,占营收17%,相比上年的28%,全年为4.65-4.75亿美元与此前一致。用户人数159,787,环比增长 4.6%

作者:简知行

链接:网页链接