导读

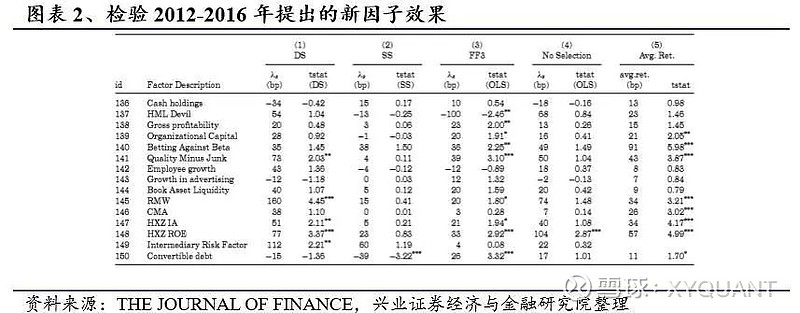

1、作为西学东渐--海外文献推荐系列报告第六十九篇,本期我们推荐了Feng G , Giglio S , Xiu D 于2020年发表的论文《Taming the Factor Zoo: A Test of New Factors》。

2、本文指出对新因子有效性进行评估的传统方法受模型选择错误影响较大,这使得对新因子的评估结果并不准确。本文创新性地基于目前较为前沿的计量经济学方法提出了一套系统化评估新因子对资产定价贡献的框架,同时该框架也可以很好的应用于高维数据。

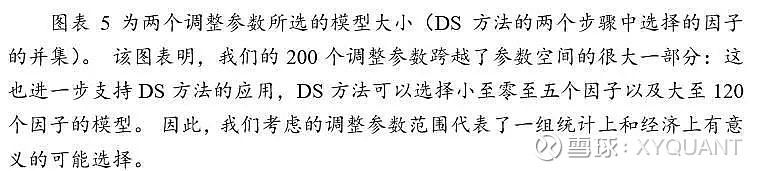

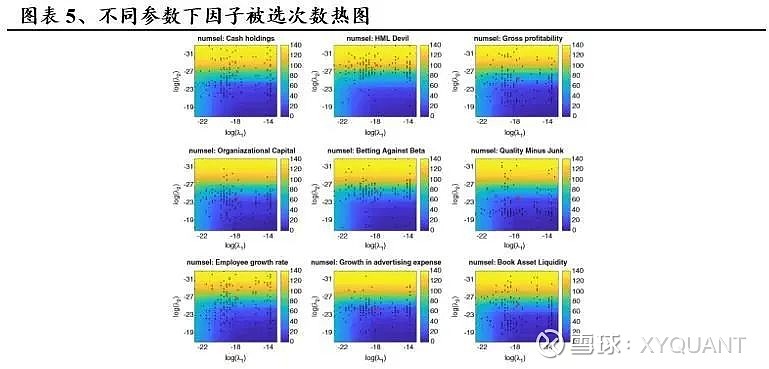

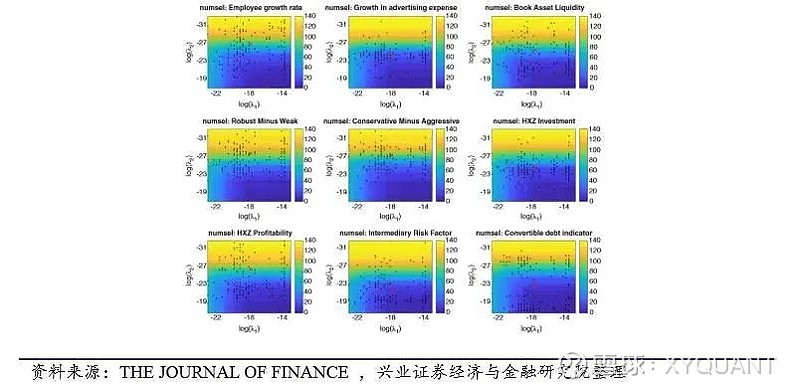

3、本文的方法不再需要对控制变量进行先验假设(如三因子模型),而是采用双重筛选Lasso回归从因子库中挑选出对横截面预期收益有解释能力的因子,这大大缓解了变量遗漏问题。通过对上百个美国市场股票因子的实证分析,文章发现大部分最近五年(2012-2016)发现的因子是冗余或无效的,仅有小部分因子对资产定价有边际上的贡献。同时文章还构建了两种递归方法对海量因子库进行降维,解决了因子数量不断增长所带来的问题。最后作者对本文所提出的方法进行了全面的稳健性测试,对最终结论提供了进一步的支持。

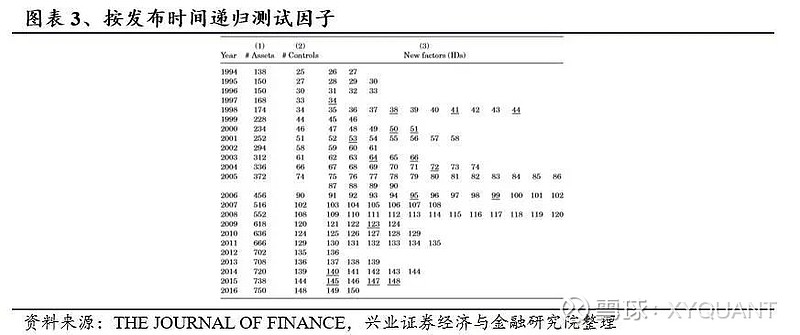

4、随着因子投资的兴起,新因子的挖掘成为学术界和业界的重点研究方向之一。然而目前对于新因子的贡献的检验可能并不适用于高维数据,同时无法很好的度量新因子在现有因子基础上的边际贡献。本文的方法对因子库的构建有着重要指导意义,可以帮助投资者更好把握新因子的作用。

风险提示:文献中的结果均由相应作者通过历史数据统计、建模和测算完成,在政策、市场环境发生变化时模型存在失效的风险。

1、引言

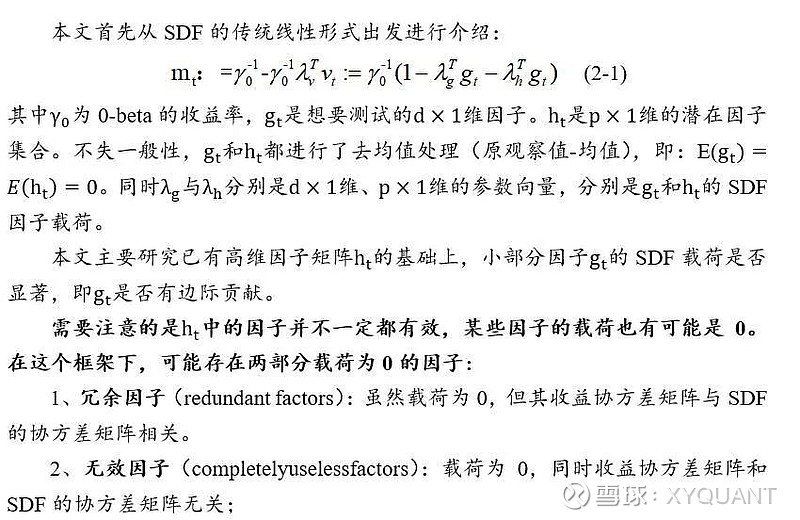

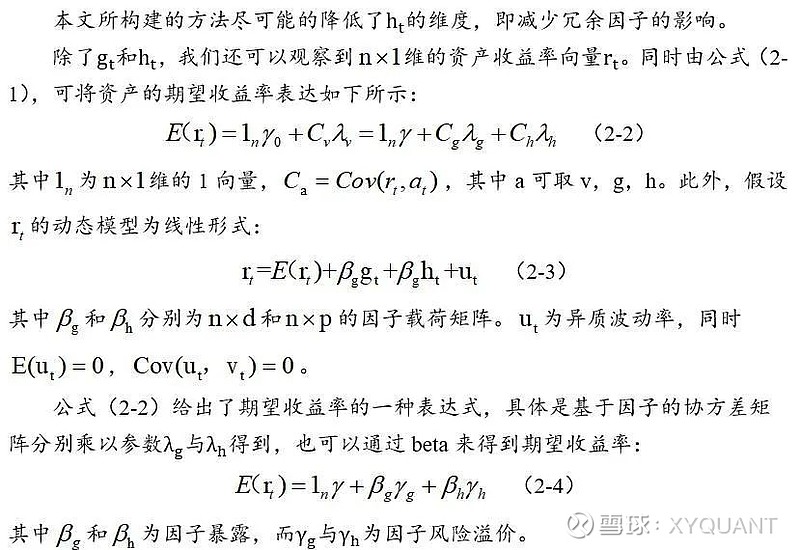

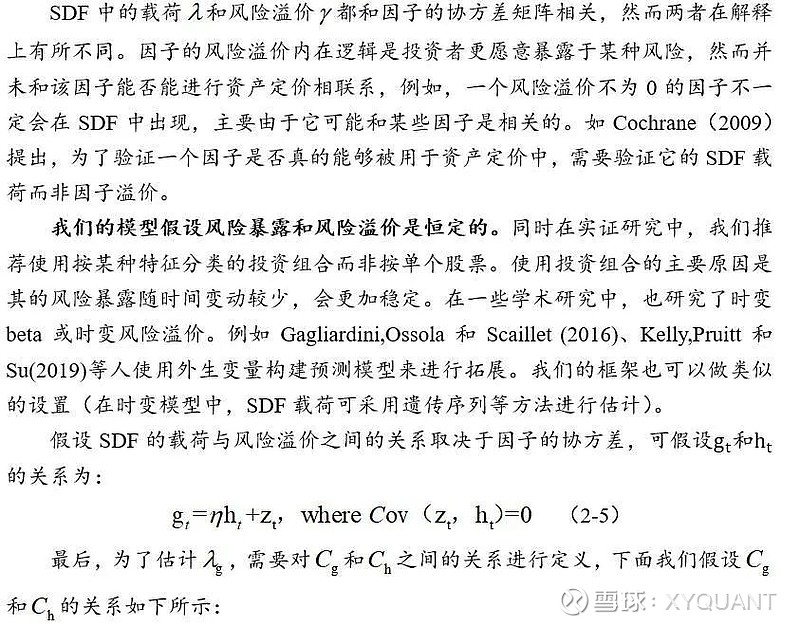

2、本文理论模型

2.1

基础模型介绍

2.2

传统方法缺点

2.3

改进思路

2.4

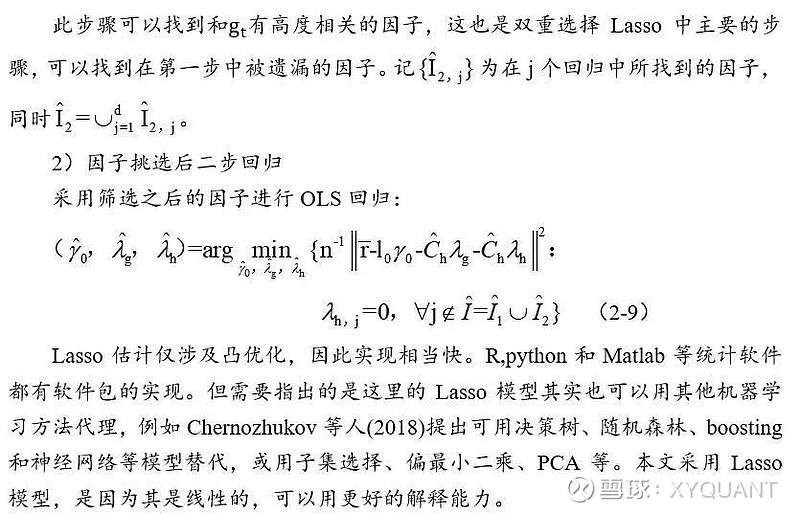

基于双重选择Lasso的两步骤回归

2.5

最优因子投资组合

3、获取风险溢价

3.1

数据

3.1.1 因子池

3.1.2测试投资组合构建

3.2

新因子评估

3.2.1 第一步Lasso回归

3.2.2 第二步Lasso回归

3.2.3 双重选择估计

3.2.4 递归法因子评价

3.2.5 逐步回归方法

3.3

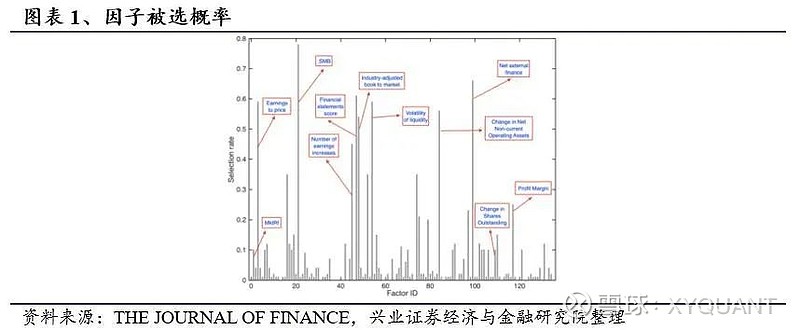

稳健性检验

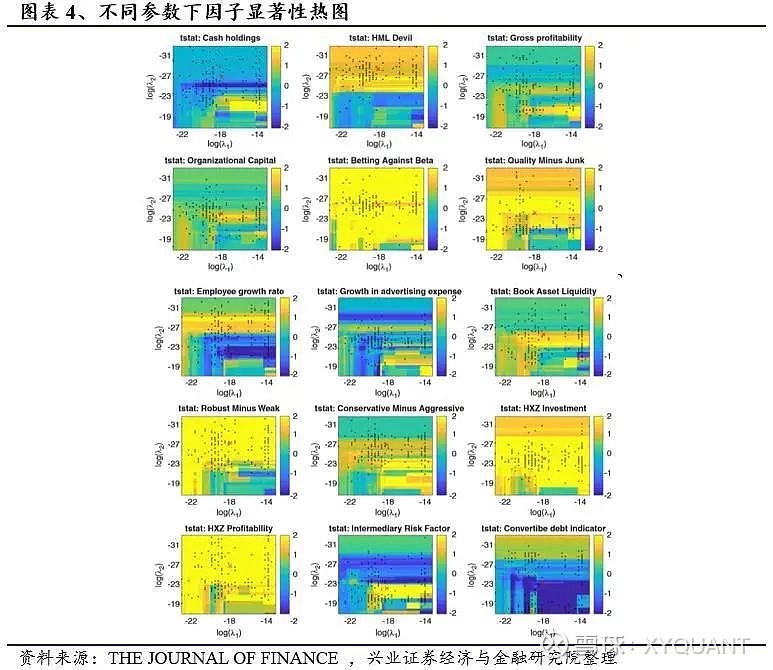

3.3.1模型参数稳健性检验

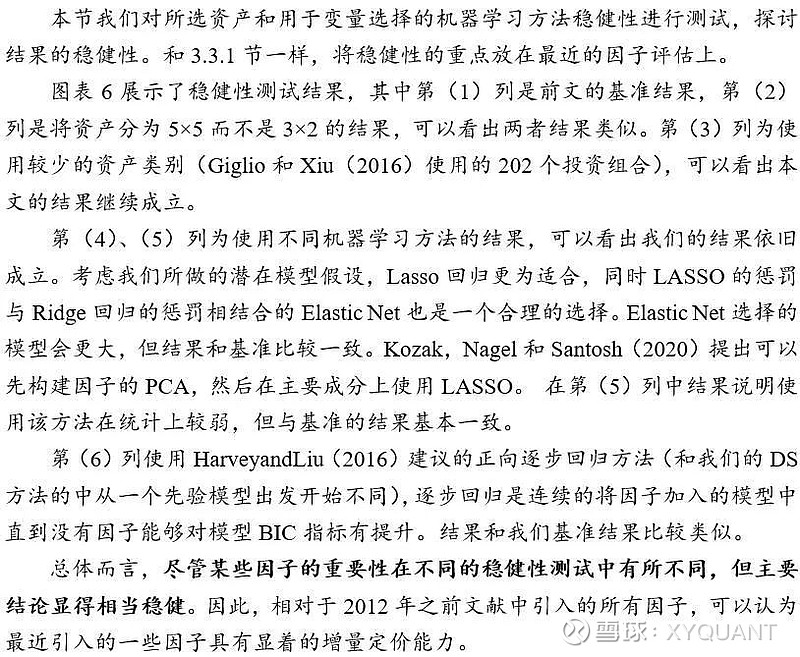

3.3.2 所选资产和正则化方法的稳健性检验

4、结论

附录

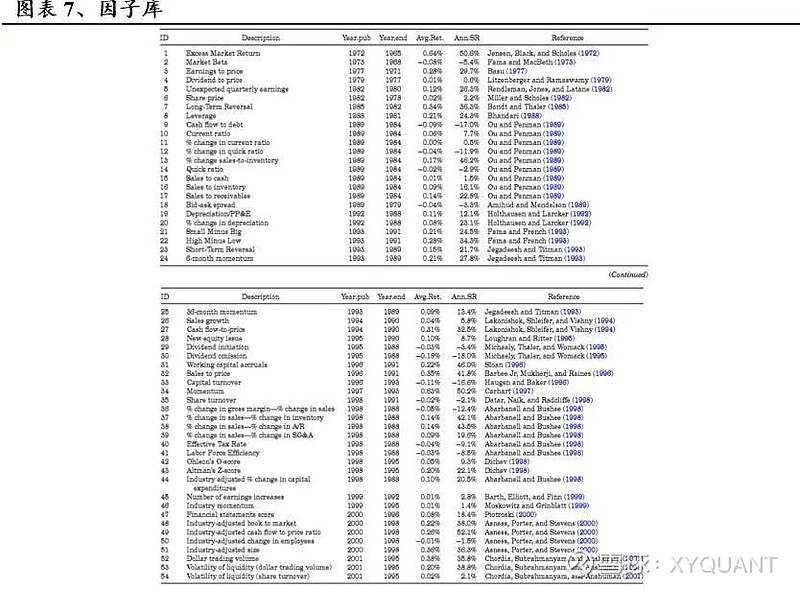

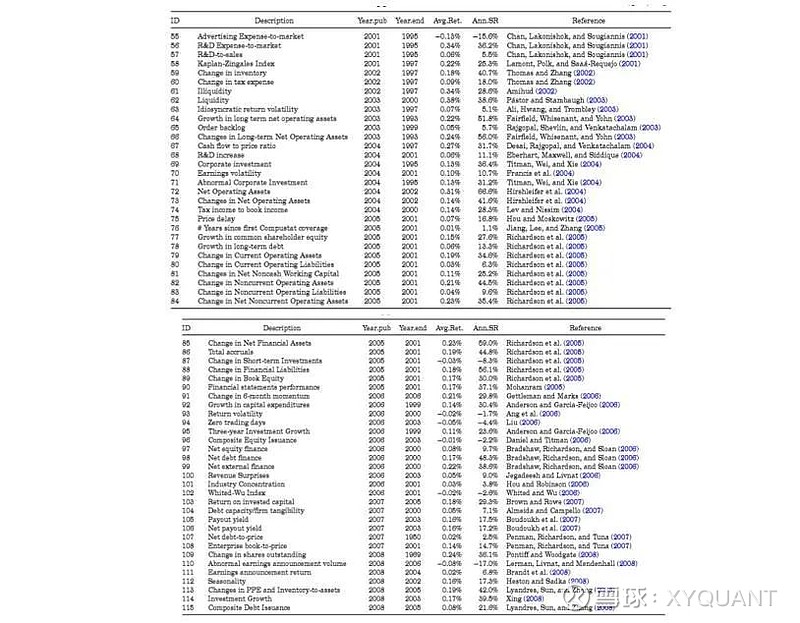

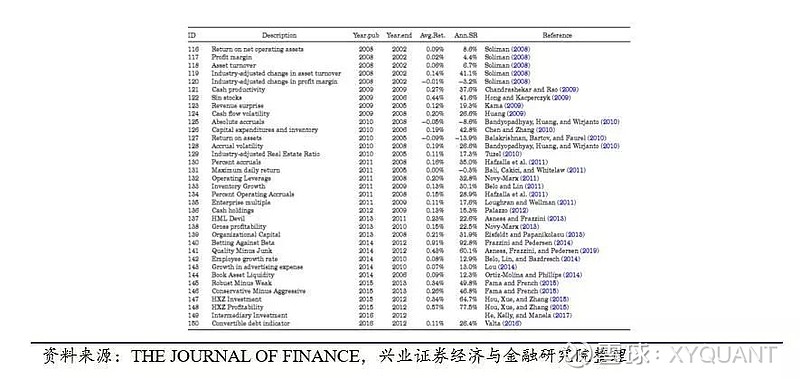

本文所构建因子库如下所示:

参考文献

[1] Abarbanell, Jeffery S., and Brian J. Bushee, 1998, Abnormal returns to a fundamental analysis strategy, The Accounting Review 73, 19–45.

[2] Adrian, Tobias, Erkko Etula, and Tyler Muir, 2014, Financial intermediaries and the cross-section of asset returns, Journal of Finance 69, 2557–2596.

[3] Ali, Ashiq, Lee-Seok Hwang, and Mark A. Trombley, 2003, Arbitrage risk and the book-to-market anomaly, Journal of Financial Economics 69, 355–373.

[4] Almeida, Heitor, and Murillo Campello, 2007, Financial constraints, asset tangibility, and corporate investment, Review of Financial Studies 20, 1429–1460.

[5] Amihud, Yakov, 2002, Illiquidity and stock returns: Cross-section and time-series effects, Journal of Financial Markets 5, 31–56.

[6] Amihud, Yakov, and Haim Mendelson, 1989, The effects of beta, bid-ask spread, residual risk, and size on stock returns, Journal of Finance 44, 479–486.

[7] Anderson,ChristopherW.,andLuisGarciaFeijoo,2006,Empiricalevidenceoncapitalinvestment, growth options, and security returns, Journal of Finance 61, 171–194.

[8] Ang, Andrew, Robert J. Hodrick, Yuhang Xing, and Xiaoyan Zhang, 2006, The cross-section of volatility and expected returns, Journal of Finance 61, 259–299.

[9] Asness, Clifford, and Andrea Frazzini, 2013, The devil in hml’s details, The Journal of Portfolio Management 39, 49–68.

[10] Asness, Clifford S., Andrea Frazzini, and Lasse Heje Pedersen, 2019, Quality minus junk, Review of Accounting Studies 24, 34–112.

[11] Asness, Clifford S., R. Burt Porter, and Ross L. Stevens, 2000, Predicting stock returns using industry-relative firm characteristics, Technical report, AQR Capital Investment.

[12] Bai, Jushan, and Guofu Zhou, 2015, Fama-macbeth two-pass regressions: Improving risk premia estimates, Finance Research Letters 15, 31–40.

[13] Balakrishnan, Karthik, Eli Bartov, and Lucile Faurel, 2010, Post loss/profit announcement drift, Journal of Accounting and Economics 50, 20–41.

[14] Bali, Turan G., Nusret Cakici, and Robert F. Whitelaw, 2011, Maxing out: Stocks as lotteries and the cross-section of expected returns, Journal of Financial Economics 99, 427–446.

[15] Bandyopadhyay, Sati P., Alan G. Huang, and Tony S. Wirjanto, 2010, The accrual volatility anomaly, Technical report, Working paper, University of Waterloo.

[16] Barbee Jr, William C., Sandip Mukherji, and Gary A. Raines, 1996, Do sales-price and debt-equity explain stock returns better than book-market and firm size? Financial Analysts Journal 52, 56–60.

[17] Barillas, Francisco, and Jay Shanken, 2018, Comparing asset pricing models, Journal of Finance 73, 715–754.

[18] Barth,MaryE.,JohnA.Elliott,andMarkW.Finn,1999,Marketrewardsassociatedwithpatterns of increasing earnings, Journal of Accounting Research 37, 387–413.

[19] Basu, Sanjoy, 1977, Investment performance of common stocks in relation to their price-earnings ratios: A test of the efficient market hypothesis, Journal of Finance 32, 663–682.

[20] Belloni, Alexandre, Daniel Chen, Victor Chernozhukov, and Christian Hansen, 2012, Sparse modelsandmethodsforoptimalinstrumentswithanapplicationtoeminentdomain,Econometrica 80, 2369–2429. Belloni, Alexandre, and Victor Chernozhukov, 2013, Least squares after model selection in highdimensional sparse models, Bernoulli 19, 521–547.

[21] Belloni, Alexandre, Victor Chernozhukov, and Christian Hansen, 2014a, High-dimensional methods and inference on structural and treatment effects, Journal of Economic Perspectives 28, 29–50.

[22] Belloni, Alexandre, Victor Chernozhukov, and Christian Hansen, 2014b, Inference on treatment effects after selection among high-dimensional controls, The Review of Economic Studies 81, 608–650. Belo, Frederico, and Xiaoji Lin, 2011, The inventory growth spread, Review of Financial Studies 25, 278–313.

[23] Belo, Frederico, Xiaoji Lin, and Santiago Bazdresch, 2014, Labor hiring, investment, and stock return predictability in the cross section, Journal of Political Economy 122, 129–177.

[24] Bhandari, Laxmi Chand, 1988, Debt/equity ratio and expected common stock returns: Empirical evidence, Journal of Finance 43, 507–528.

[25] Bickel, Peter J., Ya’acov Ritov, and Alexandre B. Tsybakov, 2009, Simultaneous analysis of Lasso and Dantzig selector, The Annals of Statistics 37, 1705–1732.

[26] Bondt, Werner F.M., and Richard Thaler, 1985, Does the stock market overreact? Journal of Finance 40, 793–805.

[27] Boudoukh, Jacob, Roni Michaely, Matthew Richardson, and Michael R Roberts, 2007, On the importance of measuring payout yield: Implications for empirical asset pricing, Journal of Finance 62, 877–915.

[28] Bradshaw, Mark T., Scott A. Richardson, and Richard G. Sloan, 2006, The relation between corporate financing activities, analysts’ forecasts and stock returns, Journal of Accounting and Economics 42, 53–85. Brandt, Michael W., Runeet Kishore, Pedro Santa-Clara, and Mohan Venkatachalam, 2008, Earnings announcements are full of surprises, Technical report, Duke University.

[29] Breeden, Douglas T., 1979, An intertemporal asset pricing model with stochastic consumption and investment opportunities, Journal of Financial Economics 7, 265–296.

[30] Brown,DavidP.,andBradfordRowe,2007,Theproductivitypremiuminequityreturns,Technical report, University of Wisconsin-Madison.

[31] Bryzgalova, Svetlana, 2015, Spurious factors in linear asset pricing models, Technical report, Stanford University. Carhart, Mark M., 1997, On persistence in mutual fund performance, Journal of Finance 52, 57–82.

[32] Chan, Louis KC, Josef Lakonishok, and Theodore Sougiannis, 2001, The stock market valuation of research and development expenditures, Journal of Finance 56, 2431–2456.

[33] Chandrashekar, Satyajit, and Ramesh KS Rao, 2009, The productivity of corporate cash holdings andthecross-sectionofexpectedstockreturns,Technicalreport,UniversityofTexasatAustin.

[34] Chen, Long, and Lu Zhang, 2010, A better three-factor model that explains more anomalies, Journal of Finance 65, 563–595.

[35] Chen, Nai-Fu, Richard Roll, and Stephen A. Ross, 1986, Economic forces and the stock market, Journal of Business 59, 383–403.

[36] Chernozhukov, Victor, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, and Whitney Newey, 2018, Double/debiased machine learning for treatment and structural parameters, The Econometrics Journal 21, 1–68.

[37] Chernozhukov, Victor, Christian Hansen, and Martin Spindler, 2015, Valid post-selection and post-regularization inference: An elementary, general approach, Annual Review of Economics 7, 649–688.

[38] Chordia, Tarun, Avanidhar Subrahmanyam, and V. Ravi Anshuman, 2001, Trading activity and expected stock returns, Journal of Financial Economics 59, 3–32.

[39] Cochrane, John H., 2009, Asset Pricing (Revised Edition) (Princeton University Press, Princeton, NJ).

[40] Cochrane, John H., 2011, Presidential address: Discount rates, Journal of Finance 66, 1047–1108. Connor, Gregory, Matthias Hagmann, and Oliver Linton, 2012, Efficient semiparametric estimation of the Fama–French model and extensions, Econometrica 80, 713–754.

风险提示:文献中的结果均由相应作者通过历史数据统计、建模和测算完成, 在政策、市场环境发生变化时模型存在失效的风险。

海外文献推荐系列第六十八期:如何根据不同的经济环境进行资产配置?

海外文献推荐系列第六十七期:最差时期的最佳策略:投资组合能否抵御危机?

海外文献推荐系列第六十六期:基于市场状态转换的动态资产配置

海外文献推荐系列第六十五期:提升因子模型的定价能力

海外文献推荐系列第六十四期:盈余公告后漂移中的价格跳跃

海外文献推荐系列第六十三期:基于参数化策略的因子测试框架

海外文献推荐系列第六十二期:预测股票市场收益:分项加总的效果优于整体

海外文献推荐系列第六十一期:基于共同基金业绩分析羊群行为能否展示基金经理能力

海外文献推荐系列第六十期:基于预期收益的风险平价模型的构建与改进

海外文献推荐系列第五十九期:基于机器学习方法的宏观因子模拟投资组合构建

海外文献推荐系列第五十八期:现金指标是否比利润指标更能预测收益?

海外文献推荐系列第五十七期:如何将因子信息融入到指数基金和主动基金之中

海外文献推荐系列第五十六期:全球区域配置框架:构建全球FOF型ETF

海外文献推荐系列第五十五期:基于宏观经济因子的战术资产配置

海外文献推荐系列第五十四期:公司治理、ESG与全球股票收益关系

海外文献推荐系列第五十三期:协方差矩阵预测方法的比较

海外文献推荐系列第五十二期:如何有效利用ESG数据构建Smart Beta指数

海外文献推荐系列第五十一期:风险轮动中的风险规避

海外文献推荐系列第五十期:基于风险溢价的投资组合—一类风险分散的新方法

海外文献推荐系列第四十九期:横截面收益中的稀疏信号研究

海外文献推荐系列第四十八期:基于机构投资者交易情绪的动态资产配置研究

海外文献推荐系列第四十七期:主动投资中的 Timing 与 Sizing

海外文献推荐系列第四十六期:市场对称性及其在组合选择中的运用

海外文献推荐系列第四十五期:股票、债券和因果关系

海外文献推荐系列第四十四期:如何确定股票的联动效应?基于网络模型的择时研究

海外文献推荐系列第四十三期:ESG投资基础:ESG对股票估值、风险和收益的影响研究

海外文献推荐系列第四十二期:使用机器学习方法预测基金持

海外文献推荐系列第四十一期:防御性宏观因子择时研究

海外文献推荐系列第四十期:股票收益的周内效应研究

海外文献推荐系列第三十九期:战术性资产配置的宏观经济仪表盘

海外文献推荐系列第三十八期:宏观量化投资新基础

海外文献推荐系列第三十七期:如何预测中国股市的下行拐点

海外文献推荐系列第三十六期:行业分类方法重构的有效性研究

海外文献推荐系列第三十五期:目标波动性策略最优性研究

海外文献推荐系列第三十四期:价值投资、成长投资的基本原则及“价值陷阱”的解释

海外文献推荐系列第三十三期:因子溢价与因子择时-跨越世纪的实证结果(二)

海外文献推荐系列第三十三期:因子溢价与因子择时-跨越世纪的实证结果(一)

海外文献推荐系列第三十二期:构建纯多头多因子策略:投资组合合并与信号合并

海外文献推荐系列第三十一期:如何对分析师预期数据进行建模?-基于贝叶斯方法的研究

海外文献推荐系列第三十期:什么是质量因子

注:文中报告节选自兴业证券经济与金融研究院已公开发布研究报告,具体报告内容及相关风险提示等详见完整版报告。

证券研究报告:《西学东渐--海外文献推荐系列之六十九》。

对外发布时间:2020年3月26日

报告发布机构:兴业证券股份有限公司(已获中国证监会许可的证券投资咨询业务资格)

--------------------------------------

分析师:徐寅

SAC执业证书编号:S0190514070004

电话:18602155387,021-38565949

E-mail: xuyinsh@xyzq.com.cn

--------------------------------------

联系人:郑兆磊

电话:13918491550

微信:13918491550

E-mail: zhengzhaolei@xyzq.com.cn

--------------------------------------

更多量化最新资讯和研究成果,欢迎关注我们的微信公众平台(微信号:XYZQ-QUANT)!