To the Shareholders of Berkshire Hathaway Inc.:

致伯克希尔哈撒韦有限公司的股东:

Berkshire’s gain in net worth during 2013 was $34.2 billion. That gain was after our deducting $1.8 billion of charges – meaningless economically, as I will explain later – that arose from our purchase of the minority interests in Marmon and Iscar. After those charges, the per-share book value of both our Class A and Class B stock increased by 18.2%. Over the last 49 years (that is, since present management took over), book value has grown from $19 to $134,973, a rate of 19.7% compounded annually.*

2013 年,伯克希尔的净值增长了 342 亿美元。这是抵消了 18 亿美元的账面冲销后的数据,账面冲销源于我们购买 Marmon 和 Iscar 的少数股权——这些冲销没有实质上的经济意义,我后面会解释。扣除上述摊销费用后,伯克希尔的 A 级和 B 级股票每股账面价值增长了 18.2%。过去的 49 年(即从现任的管理层接手以来),我们的每股账面价值从 19 美元增长到 134,973美元,复合增长率 19.7%。

On the facing page, we show our long-standing performance measurement: The yearly change inBerkshire’s per-share book value versus the market performance of the S&P 500. What counts, of course, is per share intrinsic value. But that’s a subjective figure, and book value is useful as arough tracking indicator. (An extended discussion of intrinsic value is included in our Owner-Related Business Principles on pages 103 - 108. Those principles have been included in

our reports for 30 years, and we urge new and prospective shareholders to read them.)封面上是我们的业绩衡量标准:每年伯克希尔每股账面价值的变动和标普 500 指数的比较。当然真正有意义的是每股内在价值。但内资价值是一个主观的数字,每股账面价值则是内在 价值一个有用的参考。(关于内在价值,更详细的讨论请参考我们的股东手册 103-108 页。30 多年来,这些原则一直印在我们的股东手册上,我们希望新加入的以及有兴趣成为股东 的投资者都阅读这部分内容。)

As I’ve long told you, Berkshire’s intrinsic value far exceeds its book value. Moreover, the difference has widened considerably in recent years. That’s why our 2012 decision to authorizethe repurchase of shares at 120% of book value made sense. Purchases at that level benefit continuing shareholders because per-share intrinsic value exceeds that percentage of book value by a meaningful amount. We did not purchase shares during 2013, however, because the stock price did not descend to the 120% level. If it does, we will be aggressive.我已经说过,伯克希尔的内在价值远超账面价值。并且两者之间的差距近年来显著扩大。这 也是我们在 2012 年以账面价值 120%的价格回购公司股票的原因。在这个价位回购股票有利 于继续持有的股东,因为公司的每股内在价值超过了账面价值一大截。2013 年我们没有回 购股票,原因是股价一直没有掉到账面价值 120%的价位。要不然我们会积极回购的。

Charlie Munger, Berkshire’s vice chairman and my partner, and I believe both Berkshire’s book value and intrinsic value will outperform the S&P in years when the market is down ormoderately up. We expect to fall short, though, in years when the market is strong – as we did in 2013. We have underperformed in ten of our 49 years, with all but one of our shortfalls occurring when the S&P gain exceeded 15%.公司的副董事长,我的合伙人,查理·芒格和我都相信,在市场下跌或者上涨缓慢的年份,伯克希尔的账面价值和内在价值增速都会战胜标普指数。在市场强势上涨的年份——比如刚 刚过去的 2013 年,我们一般会暂时落后。过去 49 年里,我们曾有 10 年跑输市场,其中只 有一次标普指数上涨不到 15%。

Over the stock market cycle between year ends 2007 and 2013, we overperformed the S&P. Through full cycles in future years, we expect to do that again. If we fail to do so, we will not have earned our pay. After all, you could always own an index fund and be assured of S&P results. 2007-2013 年这个周期里,我们成功跑赢了标普指数。在未来的周期中,我们也一样会跑赢 市场。如果没有做到这一点,我们将愧对于自己的工资。因为大家始终可以买一只指数基金 来获得和标普 500 一样的收益。

The Year at Berkshire今年的伯克希尔

On the operating front, just about everything turned out well for us last year – in certain cases very well. Let me count the ways:运营方面,过去的一年结果很不错——某些方面甚至非常棒。请看下文:

We completed two large acquisitions, spending almost $18 billion to purchase all of NV Energy and a major interest in H. J. Heinz. Both companies fit us well and will be prospering a century from now.

我们完成了两项大型收购,花了 180 亿美元完全买下 NV Energy,以及亨氏(H.J. Heinz)2的大笔股权。两家公司和我们都非常契合,而且它们的生意都还会红火一个世纪。

With the Heinz purchase, moreover, we created a partnership template that may be used by Berkshire in future acquisitions of size. Here, we teamed up with investors at 3G

Capital, a firm led by my friend, Jorge Paulo Lemann. His talented associates – Bernardo Hees, Heinz’s new CEO, and Alex Behring, its Chairman – are responsible for operations.在亨氏的收购中,我们创造了一个未来伯克希尔可能还会使用的合作模式。具体来说,我们和 3G Capital 的投资者合作完成了收购。3G Capital 是由我的朋友 Jorge Paulo Lemann3领导的一家公司。他的天才合伙人——Bernardo Hees,亨氏的新 CEO,以及Alex Behring,公司的董事长,将会负责公司未来的运营。

Berkshire is the financing partner. In that role, we purchased $8 billion of Heinz preferred stock that carries a 9% coupon but also possesses other features that should increase thepreferred’s annual return to 12% or so. Berkshire and 3G each purchased half of the Heinz common stock for $4.25 billion.伯克希尔扮演的角色是财务合伙人。作为财务合伙人,我们花 80 亿美元买下了亨氏 分红率 9%的优先股,并且有权利将每年优先回报提高到 12%。同时伯克希尔和 3G分别出资 42.5 亿美元各买下亨氏一半的普通股。

Though the Heinz acquisition has some similarities to a “private equity” transaction, thereis a crucial difference: Berkshire never intends to sell a share of the company. What we would like, rather, is to buy more, and that could happen: Certain 3G investors may sell some or all of their shares in the future, and we might increase our ownership at such times. Berkshire and 3G could also decide at some point that it would be mutually beneficial if we were to exchange some of our preferred for common shares (at an equity valuation appropriate to the time).我们对亨氏的收购看起来和“私募股权”投资的交易非常相似,但是有着本质的不同: 伯克希尔不打算卖出公司的任何股份。我们喜欢的是购买更多的股份,而且那很可能 发生:3G 的部分投资者将来会把他们的股份转让给我们,于是我们可以提高持股比 例。另外,伯克希尔可以和 3G 协商,在未来某个合适的时间,在对双方都有利的情 况下,将我们的优先股转换为普通股(以当时一个合理的估值)。

Our partnership took control of Heinz in June, and operating results so far are

encouraging. Only minor earnings from Heinz, however, are reflected in those we report for Berkshire this year: One-time charges incurred in the purchase and subsequent restructuring of operations totaled $1.3 billion. Earnings in 2014 will be substantial.(去年)6 月,我们的合作伙伴接手了亨氏,业绩喜人。但是在伯克希尔的报表上,来自亨氏的利润很小,这是由于收购和业务重组形成了 13 亿美元的一次性摊销。2014年的业绩数字就会变得非常明显。

With Heinz, Berkshire now owns 8.5 companies that, were they stand-alone businesses, would be in the Fortune 500. Only 491.5 to go.

有了亨氏以后,世界 500 强公司里,伯克希尔已经拥有了 8.5 家公司(忽略关联关系 将它们看作独立的公司)。现在还剩 491.5 家等着我们。

NV Energy, purchased for $5.6 billion by MidAmerican Energy, our utility subsidiary, supplies electricity to about 88% of Nevada’s population. This acquisition fits nicely intoour existing electric-utility operation and offers many possibilities for large investments in renewable energy. NV Energy will not be MidAmerican’s last major acquisition.NV Energy,由中美洲能源以 56 亿美元买下,隶属于我们的公共事业板块,为内华达 州 88%的人口供电。这笔收购和我们现有的电力事业相辅相成,并且给我们在可再生 能源的几个大项目提供了许多机会。NV Energy 不会是中美洲能源的最后一个大型收 购。

MidAmerican is one of our “Powerhouse Five” – a collection of large non-insurance businesses that, in aggregate, had a record $10.8 billion of pre-tax earnings in 2013, up $758 million from 2012. The other companies in this sainted group are BNSF, Iscar, Lubrizol and Marmon.MidAmerican Energy4(中美洲能源)是我们的“五驾马车”之一——我们最大的 5家非保险公司。2013 年中美洲能源税前利润创纪录地达到 108 亿美元,而 2012 年仅有 7.58 亿。其他的 4 架马车分别是 BNSF(伯灵顿北方圣特菲铁路公司)、Iscar(伊斯卡)6、Lubrizol(路博润)7和 Marmon8

Of the five, only MidAmerican, then earning $393 million pre-tax, was owned by Berkshire nine years ago. Subsequently, we purchased another three of the five on an all-cash basis. In acquiring the fifth, BNSF, we paid about 70% of the cost in cash, and, for the remainder, issued shares that increased the number outstanding by 6.1%. In other words, the $10.4 billion gain in annual earnings delivered Berkshire by the five companies over the nine-year span has been accompanied by only minor dilution. That satisfies our goal of not simply growing, but rather increasing per-share results.

5 架马车中,只有中美洲能源是 9 年前伯克希尔就已经拥有的,当时它税前利润 3.93亿。后来,我们相继以现金收购了另外 3 家。收购第五家,也就是 BNSF 的时候,我 们支付了 70%的现金,剩余部分通过增发股票支付,这样我们增发了 6.1%的股份。换句话说,现在 5 驾马车每年贡献给伯克希尔的 104 亿利润,而我们的股票这 9 年来 却只有轻微的稀释。这与我们不单单追求增长,而是要追求每股价值的增长这一目标 相符。

If the U.S. economy continues to improve in 2014, we can expect earnings of our Powerhouse Five to improve also – perhaps by $1 billion or so pre-tax.

如果 2014 年美国经济继续恢复,我们预计 5 驾马车的利润也会随之增长——大致会 增加 10 亿美元左右。

Our many dozens of smaller non-insurance businesses earned $4.7 billion pre-tax last year, up from $3.9 billion in 2012. Here, too, we expect further gains in 2014.非保险业务里,我们其他小一些的公司税前盈利从 2012 年的 39 亿增长到今年的 47亿。预计 2014 年它们也会持续增长。

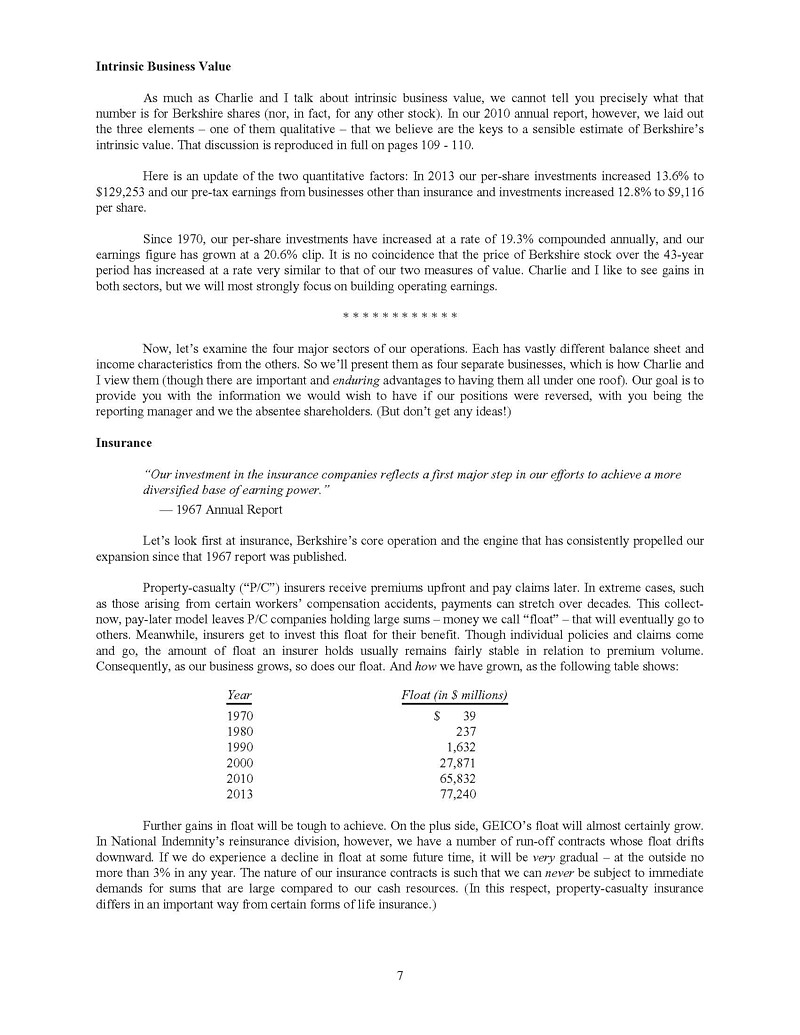

Berkshire’s extensive insurance operation again operated at an underwriting profit in2013 – that makes 11 years in a row – and increased its float. During that 11-year stretch,our float – money that doesn’t belong to us but that we can invest for Berkshire’s benefit – has grown from $41 billion to $77 billion.

2013 年,伯克希尔最重要的保险业务再次实现了承保盈利——这是连续承保盈利的 第 11 个年头了,浮存金也还在继续增加。11 年来我们的浮存金——那些不属于伯克 希尔,但是我们可以投资并未伯克希尔赚取收益的钱,从 410 亿增加到了 770 亿。

Concurrently, our underwriting profit has aggregated $22 billion pre-tax, including $3 billion realized in 2013. And all of this all began with our 1967 purchase of National Indemnity for $8.6million.

与此同时,我们累计实现了 220 亿税前承保利润,其中 2013 年 30 亿。而这一切,都起始于我们 1967 年以 860 万美元收购了 National Indemnity。

We now own a wide variety of exceptional insurance operations. Best known is GEICO, the car insurer Berkshire acquired in full at yearend 1995 (having for many years prior owned

a partial interest). GEICO in 1996 ranked number seven among U.S. auto insurers. Now, GEICO is number two, having recently passed Allstate. The reasons for this amazing

growth are simple: low prices and reliable service. You can do yourself a favor by calling 1-800-847-7536 or checking Geico.com to see if you, too, can cut your insurance costs.

Buy some of Berkshire’s other products with the savings.现在我们已经拥有多家卓越的保险公司。最为人所熟知的,GEICO, 由 1955 年伯克希 尔完全收购的车险公司(在那之前很多年我们就持有它部分权益了)。1996 年 GEICO在美国车险企业里排名第七。现在它排第二,刚刚超过了 Allstate。它惊人增长的秘 密其实非常简单:便宜的价格和可靠的服务。大家应该打客服电话 1-800-847-7536,或者登录 Geico.com,看看 GEICO 的产品是不是能帮你节省一些保险支出。省下来的 钱可以买些其他伯克希尔的产品。

While Charlie and I search for elephants, our many subsidiaries are regularly making bolt-on acquisitions. Last year, we contracted for 25 of these, scheduled to cost $3.1 billion in aggregate. These transactions ranged from $1.9 million to $1.1 billion in size. Charlie and I encourage these deals. They deploy capital in activities that fit with our existing businesses and that will be managed by our corps of expert managers. The result is no more work for us and more earnings for you. Many more of these bolt-on deals will be made in future years. In aggregate, they will be meaningful.查理和我一直在猎象,我们的公司也在不断进行补强型收购。去年我们一共有 25 笔,总计 31 亿美元的此类收购。这些收购从 190 万到 11 亿美元不等。查理和我都支持这 些收购。它们把资本用在了契合我们现有业务的地方,并且将由我们优秀的经理人团 队管理。结果就是,我们不用干活,大家却在赚钱。未来还会有更多类似的补强型收 购。整体而言,它们带来的意义非凡。

Last year we invested $3.5 billion in the surest sort of bolt-on: the purchase of additional shares in two wonderful businesses that we already controlled. In one case – Marmon –our purchases brought us to the 100% ownership we had signed up for in 2008. In the other instance – Iscar – the Wertheimer family elected to exercise a put option it held, selling us the 20% of the business it retained when we bought control in 2006.去年我们投资了 35 亿,用于确定无疑的补强型投资:购买了两家我们已经拥有控制 权公司的剩余股权。第一个是 Marmon,根据 2008 年的协议我们获得了 Marnon 100%的权益。另一个是 Iscar,Wertheimer 家族决定行使它的卖出权,将其持有公司的 20%股份转让给我们。2006 年我们已经获得了公司的控制权。

These purchases added about $300 million pre-tax to our current earning power and also delivered us $800 million of cash. Meanwhile, the same nonsensical accounting rule that Idescribed in last year’s letter required that we enter these purchases on our books at $1.8 billion less than we paid, a process that reduced Berkshire’s book value. (The charge wasmade to “capital in excess of par value”; figure that one out.) This weird accounting, youshould understand, instantly increased Berkshire’s excess of intrinsic value over book value by the same $1.8 billion.

两笔收购让我们增加了 3 亿的税前利润,带来 8 亿的现金流。但是去年的信中已经讲 过的,“虚幻”的会计准则要求我们以低于支付金额 18 亿的价格对它入账,于是减少 了伯克希尔的账面价值。(这项费用应该记在“超过账面价值的资本”项目下;一个 报表上没有的项目)。大家应该明白,这条怪异的会计要求使得伯克希尔内在价值和 账面价值的差距增加了 18 亿。

Our subsidiaries spent a record $11 billion on plant and equipment during 2013, roughly twice our depreciation charge. About 89% of that money was spent in the United States. Though we invest abroad as well, the mother lode of opportunity resides in America. 2013 年,伯克希尔所属企业在厂房、设备上的资本开支达到 110 亿,几乎是折旧额 的 2 倍。大约 89%的钱投在了美国。我们也在国外投资,但是投资机会的主矿脉还是 在美国。

In a year in which most equity managers found it impossible to outperform the S&P 500, both Todd Combs and Ted Weschler handily did so. Each now runs a portfolio exceeding$7 billion. They’ve earned it.

去年多数投资经理没能战胜标普 500,但是 Todd Combs 和 Ted Weschler 轻松做到了。他们各自管理的组合都超过了 70 亿美元。他们应得的。

I must again confess that their investments outperformed mine. (Charlie says I should add“by a lot.”) If such humiliating comparisons continue, I’ll have no choice but to ceasetalking about them.我不得不坦白,他们的投资业绩超过了我。(查理提醒我应该加上“超过了一大截”。) 如果这种令人惭愧的对比继续下去,我就只好闭口不提他俩了。

Todd and Ted have also created significant value for you in several matters unrelated to their portfolio activities. Their contributions are just beginning: Both men have Berkshire blood in their veins.除了投资赚钱以外,Todd 和 Ted 还在诸多方面为大家创造了价值。他们带来的价值 只是小荷才露尖尖角:他们都流淌着伯克希尔的血。

Berkshire’s yearend employment – counting Heinz – totaled a record 330,745, up 42,283 from last year. The increase, I must admit, included one person at our Omaha home office.(Don’t panic: The headquarters gang still fits comfortably on one floor.)截至年底,伯克希尔的雇员总数,算上亨氏,再创纪录达到了 330,745 人,比去年增 加了 42,283 人。我得承认,增加的人里包括一名在奥马哈家庭办公室里上班的人。(别 慌:一层楼还是足够公司总部的家伙们用了,不挤。)

Berkshire increased its ownership interest last year in each of its “Big Four” investments –American Express, Coca-Cola, IBM and Wells Fargo. We purchased additional shares of Wells Fargo (increasing our ownership to 9.2% versus 8.7% at yearend 2012) and IBM (6.3% versus 6.0%). Meanwhile, stock repurchases at Coca-Cola and American Express raised

our percentage ownership. Our equity in CocaCola grew from 8.9% to 9.1% and our interest in American Express from 13.7% to 14.2%. And, if you think tenths of a percentaren’t important, ponder this math: For the four companies in aggregate, each increase of one-tenth of a percent in our share of their equity raises Berkshire’s share of their annualearnings by $50 million.去年伯克希尔在“四大”上的投资比例都上升了——美国运通、可口可乐、IBM 和富 国银行。我们增持了富国银行(从 2012 年底的 8.7%增加到 9.2%)和 IBM(从 6.0%到 6.3%)。同时,可口可乐和美国运通的股票回购提高了我们的持股比例。我们在可 口可乐的持股比例从 8.9%提高到 9.1%,美国运通的从 13.7%提高到 14.2%。如果大家 觉得百分之零点几的变动意思不大,那请大家这样估算一下:我们在四大上的投资,每增加 0.1%,伯克希尔每年的利润就会增加 5000 万。

The four companies possess excellent businesses and are run by managers who are both talented and shareholder-oriented. At Berkshire, we much prefer owning a

non-controlling but substantial portion of a wonderful company to owning 100% of a

so-so business; it’s better to have a partial interest in the Hope diamond than to own all

of a rhinestone.四家公司都拥有良好的业务,并由聪明而且为股东着想的经理人掌管。在伯克希尔,我们情愿拥有一家好公司非控制性但大比例的持股,也不愿意 100%拥有一家普普通 通的公司;宁愿拥有希望之星的一部分,也不愿要一整颗人造钻石,同样的道理。

Going by our yearend holdings, our portion of the “Big Four’s” 2013 earnings amountedto $4.4 billion. In the earnings we report to you, however, we include only the dividends we receive – about $1.4 billion last year. But make no mistake: The $3 billion of theirearnings we don’t report is every bit as valuable to us as the portion Berkshire records.以年末的持股比例计算,2013 年四大归属于我们的利润 44 亿。但是在利润表上,我 们只报告了分红——大约 14 亿。但是别犯迷糊:没有报告的 30 亿利润每一分都和账 上报告的一样值钱。

The earnings that these four companies retain are often used for repurchases of their own stock – a move that enhances our share of future earnings – as well as for funding business opportunities that usually turn out to be advantageous. All that leads us to expect that the per-share earnings of these four investees will grow substantially over time. If they do, dividends to Berkshire will increase and, even more important, our unrealized capital gains will, too. (For the four, unrealized gains already totaled $39 billion at yearend.)

4 家公司留存的利润经常被用于回购股票——这将增加未来我们所占的利润比例,或 者投资于有利可图的新业务。可以预期,我们在“四大”上的每股投资利润都会不断 显著增长。倘若事实的确如此,伯克希尔获得的分红也将随之增加,更重要的是,我 们的未实现资本收益也会增长。(截止年底,我们在“四大”上的未实现收益累计 390亿美元。)

Our flexibility in capital allocation – our willingness to invest large sums passively in on-controlled businesses – gives us a significant advantage over companies that limit themselves to acquisitions they can operate. Woody Allen stated the general idea whenhe said: “The advantage of being bi-sexual is that it doubles your chances for a date on Saturday night.” Similarly, our appetite for either operating businesses or passive investments doubles our chances of finding sensible uses for our endless gusher of cash.相比于那些局限于投资自身能够运营的业务的公司,我们在投资上的灵活性——大额 进行被动投资的意愿,让我们拥有更多优势。伍迪·艾伦说过,“双性恋的好处就是,周六晚上约会的概率可以提高一倍。”同样,我们即投资可以自己运营的业务,又愿 意被动投资,于是我们源源不断的现金找寻到合适投资机会的概率也提高了一倍。

************

Late in 2009, amidst the gloom of the Great Recession, we agreed to buy BNSF, the largest

purchase in Berkshire’s history. At the time, I called the transaction an “all-in wager on the economic future of the United States.”

2009 年年末,在大衰退的阴影中,我们通过了买下 BNSF 的决定,伯克希尔历史上最大的收 购。当时我把这笔交易称作是“完全下注于美国经济的赌博”。

That kind of commitment was nothing new for us: We’ve been making similar wagers ever since Buffett Partnership Ltd. acquired control of Berkshire in 1965. For good reason, too. Charlie and I have always considered a “bet” on ever-rising U.S. prosperity to be very close to a sure thing.当然这对我们来说也不是新鲜事了:从巴菲特合伙公司 1965 年买下伯克希尔以来,我们一 直在下类似的赌注。以同样充分的理由。查理和我一直认为“赌”美国长盛不衰,几乎是一 件只赚不赔的事。

Indeed, who has ever benefited during the past 237 years by betting against America? If you compare our country’s present condition to that existing in 1776, you have to rub your eyes in wonder. And the dynamism embedded in our market economy will continue to work its magic.America’s best days lie ahead.

过去的 237 年里看空美国的人中谁获益了?如果把我们国家现在的样子和 1776 年作一个比 较,大家一定不敢相信自己的眼睛。而且市场经济的内在机制还会继续发挥它的魔力,美国 的好日子还在前头。

With this tailwind working for us, Charlie and I hope to build Berkshire’s per-share intrinsic value by (1) constantly improving the basic earning power of our many subsidiaries; (2) further increasing their earnings through bolt-on acquisitions; (3) benefiting from the growth of our investees; (4) repurchasing Berkshire shares when they are available at a meaningful discount from intrinsic value; and (5) making an occasional large acquisition. We will also try to maximize results for you by rarely, if ever, issuing Berkshire shares. Those building blocks rest on a rock-solid foundation. A century hence, BNSF and MidAmerican Energy will still be playing major roles in our economy. Insurance will concomitantly be essential for both businesses and individuals – and no company brings greater human and financial resources to that business than Berkshire.趁着顺风,查理和我希望通过以下方式更进一步增加伯克希尔的每股内在价值:1、持续增 强各个业务公司的盈利能力;2、继续通过补强型收购来增加它们的利润;3、从我们投资的 公司的增长中获益;4、当伯克希尔的股价下跌到相对内在价值有很大折扣时回购公司股票;5、偶尔进行大型的收购。少数情况下,我们也可能通过增发伯克希尔的股票来最大化大家 的收益。这些方式都有其坚实的基础。一个世纪内,BNSF 和中美洲能源还将继续在我们的 经济中扮演重要角色。无论对于公司还是个人,保险业务也依然不可或缺,在这方面,伯克 希尔投入的人力和资金超过其他任何公司。

Moreover, we will always maintain supreme financial strength, operating with at least $20 billion of cash equivalents and never incurring material amounts of short-term obligations. As we view these and other strengths, Charlie and I like your company’s prospects. We feel fortunate to be entrusted with its management.

另外,我们依然会保持高度的财务稳健,维持至少 200 亿的现金及等价物,并避免承担大规 模的短期债务。考虑到方方面面的优势,查理和我非常看好公司的未来。我们感到非常幸运 能够将财富托付给公司管理。

Intrinsic Business Value内在价值

As much as Charlie and I talk about intrinsic business value, we cannot tell you precisely what that number is for Berkshire shares (nor, in fact, for any other stock). In our 2010 annual report, however, we laid out the three elements – one of them qualitative – that we believe are the keys to a sensible estimate of Berkshire’s intrinsic value. That discussion is reproduced in full on pages 109 - 110.查理和我时常提到内在价值,但是我们很难告诉大家伯克希尔每股内在价值的准确数字(实 际上,其他任何股票都不能)。2010 年的年报中,我们提出了三个基本要素——其中一个是 定性的,我们相信这些要素是衡量伯克希尔内在价值的关键指标。这些讨论我们完整地收录 在 109-110 页。

Here is an update of the two quantitative factors: In 2013 our per-share investments increased 13.6% to $129,253 and our pre-tax earnings from businesses other than insurance and investments increased 12.8% to $9,116 per share.

这里是我们对两个定量指标的更新:2013 年,我们的每股投资增长了 13.6%至 129,253,另 外我们的非保险非投资业务每股税前利润增长了 12.8%至 9,116。

Since 1970, our per-share investments have increased at a rate of 19.3% compounded annually, and our earnings figure has grown at a 20.6% clip. It is no coincidence that the price of Berkshire stock over the 43-year period has increased at a rate very similar to that of our two measures of value. Charlie and I like to see gains in both sectors, but we will most strongly focus on building operating earnings.

1970 年来,我们的每股投资以每年 19.3%的速度复合增长,同时我们的运营利润数增速是20.6%。伯克希尔的股价 43 年来以一个类似的速度增长并非巧合。查理和我喜欢看到两个部 分都获得增长,但是我们会更在意运营利润。

************

Now, let’s examine the four major sectors of our operations. Each has vastly different balancesheet and income characteristics from the others. So we’ll present them as four separatebusinesses, which is how Charlie and I view them (though there are important and enduring advantages to having them all under one roof). Our goal is to provide you with the information we would wish to have if our positions were reversed, with you being the reporting manager andwe the absentee shareholders. (But don’t get any ideas!)

接下来,我们看一下公司四个主要板块的业务情况。四个板块都有完全不同的资产负债表 和收入特性。所以我们把它们区别对待,这也是查理和我看待业务的方式(但是把它们在同 一个体系中运作是非常重要并且具有优势的)。假设我们位置互换,我们自己是没到场的股 东,而大家是作报告的管理层,那提供我们想要知道的信息就是以下汇报的目标。

未完待续……

英文原版如下:

声明:本文意在传播价值,不涉及商业用途。版权归原作者所有

图文来源:网络