Our Method of Operation

In past annual letters I have always utilized three categories to describe investment operations we conduct. I now feel that a four-category division is more appropriate. Partially, the addition of a new section - "Generals Relatively Undervalued" - reflects my further consideration of essential differences that have always existed to a small extent with our "Generals" group. Partially, it reflects the growing importance of what once was a very small sub-category but is now a much more significant part of our total portfolio. This increasing importance has been accompanied by excellent results to date justifying significant time and effort devoted to finding additional opportunities in this area. Finally, it partially reflects the development and implementation of a new and somewhat unique investment technique designed to improve the expectancy and consistency of operations in this category. Therefore, our four present categories are:

1. “Generals -Private Owner Basis” - a category of generally undervalued stocks, determined by quantitative standards, but with considerable attention also paid to the qualitative factor. There is often little or nothing to indicate immediate market improvement. The issues lack glamour or market sponsorship. Their main qualification is a bargain price; that is, an overall valuation of the enterprise substantially below what careful analysis indicates its value to a private owner to be. Again, let me emphasize that while the quantitative comes first and is essential, the qualitative is important. We like good management - we like a decent industry - we like a certain amount of “ferment” in a previously dormant management or stockholder group. But, we demand value.

Many times in this category we have the desirable "two strings to our bow" situation where we should either achieve appreciation of market prices from external factors or from the acquisition of a controlling position in a business at a bargain price. While the former happens in the overwhelming majority of cases, the latter represents an insurance policy most investment operations don't have. We have continued to enlarge the positions in the three companies described in our 1964 midyear report where we are the largest stockholder. All three companies are increasing their fundamental value at a very satisfactory rate, and we are completely passive in two situations and active only on a very minor scale in the third. It is unlikely that we will ever take a really active part in policy-making in any of these three companies, but we stand ready if needed.

2. "Generals -Relatively Undervalued" - this category consists of securities selling at prices relatively cheap compared to securities of the same general quality. We demand substantial discrepancies from current valuation standards, but (usually because of large size) do not feel value to a private owner to be a meaningful concept. It is important in this category, of course, that apples be compared to apples - and not to oranges, and we work hard at achieving that end. In the great majority of cases we simply do not know enough about the industry or company to come to sensible judgments -in that situation we pass.

As mentioned earlier, this new category has been growing and has produced very satisfactory results. We have recently begun to implement a technique, which gives promise of very substantially reducing the risk from an overall change in valuation standards; e.g. I we buy something at 12 times earnings when comparable or poorer quality companies sell at 20 times earnings, but then a major revaluation takes place so the latter only sell at 10 times.

This risk has always bothered us enormously because of the helpless position in which we could be left compared to the "Generals -Private Owner" or "Workouts" types. With this risk diminished, we think this category has a promising future.

3. "Workouts" - these are the securities with a timetable. They arise from corporate activity - sell-outs, mergers, reorganizations, spin-offs, etc. In this category we are not talking about rumors or "inside information" pertaining to such developments, but to publicly announced activities of this sort. We wait until we can read it in the paper. The risk pertains not primarily to general market behavior (although that is sometimes tied in to a degree), but instead to something upsetting the applecart so that the expected development does not materialize. Such killjoys could include anti-trust or other negative government action, stockholder disapproval, withholding of tax rulings, etc. The gross profits in many workouts appear quite small. It's a little like looking for parking meters with some time left on them. However, the predictability coupled with a short holding period produces quite decent average annual rates of return after allowance for the occasional substantial loss. This category produces more steady absolute profits from year to year than generals do. In years of market decline it should usually pile up a big edge for us; during bull markets it will probably be a drag on performance. On a long-term basis, I expect the workouts to achieve the same sort of margin over the Dow attained by generals.

4. "Controls" - these are rarities, but when they occur they are likely to be of significant size. Unless we start off with the purchase of a sizable block of stock, controls develop from the general - private owner category. They result from situations where a cheap security does nothing pricewise for such an extended period of time that we are able to buy a significant percentage of the company's stock. At that point we are probably in a position to assume a degree of or perhaps complete control of the company's activities. Whether we become active or remain relatively passive at this point depends upon our assessment of the company's future and the managements capabilities.

We do not want to get active merely for the sake of being active. Everything else being equal, I would much rather let others do the work. However, when an active role is necessary to optimize the employment of capital, you can be sure we will not be standing in the wings.

Active or passive, in a control situation there should be a built-in profit. The sine qua non of this operation is an attractive purchase price. Once control is achieved, the value of our investment is determined by the value of the enterprise, not the oftentimes irrationalities of the market place.

Any of the three situations where we are now the largest stockholders mentioned under Generals - Private Owner could, by virtue of the two-way stretch they possess, turn into controls. That would suit us fine, but it also suits us if they advance in the market to a price more in line with intrinsic value enabling us to sell them, thereby completing a successful generals - private owner operation.

Investment results in the control category have to be measured on the basis of at least several years. Proper buying takes time. If needed, strengthening management, redirecting the utilization of capital, perhaps effecting a satisfactory sale or merger, etc., are also all factors that make this a business to be measured in years rather than months. For this reason, in controls, we are looking for wide margins of profit -if it appears at all close, we quitclaim.

Controls in the buying stage move largely in sympathy with the Dow. In the later stages their behavior is geared more to that of workouts.

You might be interested to know that the buyers of our former control situation, Dempster Mill Manufacturing, seem to be doing very well with it. This fulfills our expectation and is a source of satisfaction. An investment operation that depends on the ultimate buyer making a bum deal (in Wall Street they call this the "Bigger Fool Theory") is tenuous indeed. How much more satisfactory it is to buy at really bargain prices so that only an average disposition brings pleasant results.

As I have mentioned in the past, the division of our portfolio among categories is largely determined by the accident of availability. Therefore, in any given year the mix between generals, workouts, or controls is largely a matter of chance, and this fickle factor will have a great deal to do with our performance relative to the Dow.

This is one of many reasons why single year's performance is of minor importance and good or bad, should never be taken too seriously.

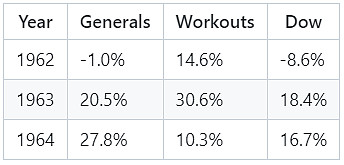

To give an example of just how important the accident of division between these categories is, let me cite the example of the past three years. Using an entirely different method of calculation than that used to measure the performance of BPL in entirety, whereby the average monthly investment at market value by category is utilized, borrowed money and office operating expenses excluded, etc., (this gives the most accurate basis for intergroup comparisons but does not reflect overall BPL results) the generals (both present categories combined), workouts, and the Dow, shape up as follows:

Obviously the workouts (along with controls) saved the day in 1962, and if we had been light in this category that year, our final result would have been much poorer, although still quite respectable considering market conditions during the year. We could just as well have had a much smaller percentage of our portfolio in workouts that year; availability decided it, not any notion on my part as to what the market was going to do. Therefore, it is important to realize that in 1962 we were just plain lucky regarding mix of categories.

In 1963 we had one sensational workout which greatly influenced results, and generals gave a good account of themselves, resulting in a banner year. If workouts had been normal, (say, more like 1962) we would have looked much poorer compared to the Dow. Here it wasn't our mix that did much for us, but rather excellent situations.

Finally, in 1964 workouts were a big drag on performance. This would be normal in any event during a big plus year for the Dow such as 1964, but they were even a greater drag than expected because of mediocre experience. In retrospect it would have been pleasant to have been entirely in generals, but we don’t play the game in retrospect.

I hope the preceding table drives home the point that results in a given year are subject to many variables - some regarding which we have little control or insight. We consider all categories to be good businesses and we are very happy we have several to rely on rather than just one. It makes for more discrimination within each category and reduces the chance we will be put completely out of operation by the elimination of opportunities in a single category.

Taxes

We have had a chorus of groans this year regarding partners' tax liabilities. Of course, we also might have had a few if the tax sheet had gone out blank.

More investment sins are probably committed by otherwise quite intelligent people because of "tax considerations" than from any other cause. One of my friends - a noted West Coast philosopher maintains that a majority of life's errors are caused by forgetting what one is really trying to do. This is certainly the case when an emotionally supercharged element like taxes enters the picture (I have another friend -a noted East Coast philosopher who says it isn't the lack of representation he minds -it's the taxation).

Let's get back to the West Coast. What is one really trying to do in the investment world? Not pay the least taxes, although that may be a factor to be considered in achieving the end. Means and end should not be confused, however, and the end is to come away with the largest after-tax rate of compound. Quite obviously if two courses of action promise equal rates of pre-tax compound and one involves incurring taxes and the other doesn't the latter course is superior. However, we find this is rarely the case.

It is extremely improbable that 20 stocks selected from, say, 3000 choices are going to prove to be the optimum portfolio both now and a year from now at the entirely different prices (both for the selections and the alternatives) prevailing at that later date. If our objective is to produce the maximum after-tax compound rate, we simply have to own the most attractive securities obtainable at current prices, And, with 3,000 rather rapidly shifting variables, this must mean change (hopefully “tax-generating” change).

It is obvious that the performance of a stock last year or last month is no reason, per se, to either own it or to not own it now. It is obvious that an inability to "get even" in a security that has declined is of no importance. It is obvious that the inner warm glow that results from having held a winner last year is of no importance in making a decision as to whether it belongs in an optimum portfolio this year.

If gains are involved, changing portfolios involves paying taxes. Except in very unusual cases (I will readily admit there are some cases), the amount of the tax is of minor importance if the difference in expectable performance is significant. I have never been able to understand why the tax comes as such a body blow to many people since the rate on long-term capital gain is lower than on most lines of endeavor (tax policy indicates digging ditches is regarded as socially less desirable than shuffling stock certificates).

I have a large percentage of pragmatists in the audience so I had better get off that idealistic kick. There are only three ways to avoid ultimately paying the tax: (1) die with the asset - and that's a little too ultimate for me even the zealots would have to view this "cure" with mixed emotions; (2) give the asset away - you certainly don't pay any taxes this way, but of course you don't pay for any groceries, rent, etc., either; and (3) lose back the gain if your mouth waters at this tax-saver, I have to admire you -you certainly have the courage of your convictions.

So it is going to continue to be the policy of BPL to try to maximize investment gains, not minimize taxes. We will do our level best to create the maximum revenue for the Treasury -at the lowest rates the rules will allow.

An interesting sidelight on this whole business of taxes, vis-à-vis investment management, has appeared in the last few years. This has arisen through the creation of so-called "swap funds" which are investment companies created by the exchange of the investment company's shares for general market securities held by potential investors. The dominant sales argument has been the deferment (deferment, when pronounced by an enthusiastic salesman, sometimes comes very close phonetically to elimination) of capital gains taxes while trading a single security for a diversified portfolio. The tax will only finally be paid when the swap fund's shares are redeemed. For the lucky ones, it will be avoided entirely when any of those delightful alternatives mentioned two paragraphs earlier eventuates.

The reasoning implicit in the swapee's action is rather interesting. He obviously doesn't really want to hold what he is holding or he wouldn't jump at the chance to swap it (and pay a fairly healthy commission - usually up to $100,000) for a grab-bag of similar hot potatoes held by other tax-numbed investors. In all fairness, I should point out that after all offerees have submitted their securities for exchange and had a chance to review the proposed portfolio they have a chance to back out but I understand a relatively small proportion do so.

There have been twelve such funds (that I know of) established since origination of the idea in 1960, and several more are currently in the works. The idea is not without appeal since sales totaled well over $600 million. All of the funds retain an investment manager to whom they usually pay 1/2 of 1% of asset value. This investment manager faces an interesting problem; he is paid to manage the fund intelligently (in each of the five largest funds this fee currently ranges from $250,000 to $700,000 per year), but because of the low tax basis inherited from the contributors of securities, virtually his every move creates capital gains tax liabilities. And, of course, he knows that if he incurs such liabilities, he is doing so for people who are probably quite sensitive to taxes or they wouldn't own shares in the swap fund in the first place.

I am putting all of this a bit strongly, and I am sure there are some cases where a swap fund may be the best answer to an individual's combined tax and investment problems. Nevertheless, I feel they offer a very interesting test-tube to measure the ability of some of the most respected investment advisors when they are trying to manage money without paying (significant) taxes.

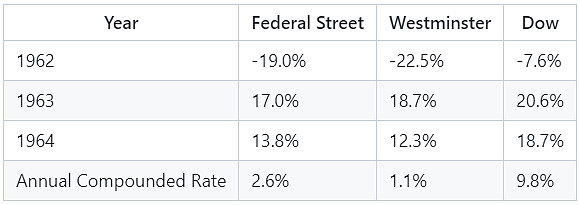

The three largest swap funds were all organized in 1961, and combined have assets now of about $300 million. One of these, Diversification Fund, reports on a fiscal year basis which makes extraction of relevant data quite difficult for calendar year comparisons. The other two, Federal Street Fund and Westminster Fund (respectively first and third largest in the group) are managed by investment advisors who oversee at least $2 billion of institutional money.

Here's how they shape up for all full years of existence:

This is strictly the management record. No allowance has been made for the commission in entering and any taxes paid by the fund on behalf of the shareholders have been added back to performance.

Anyone for taxes?

Miscellaneous

In the December 21st issue of AUTOMOTIVE NEWS it was reported that Ford Motor Co. plans to spend $700 million in 1965 to add 6,742,000 square feet to its facilities throughout the world. Buffett Partnership, Ltd., never far behind, plans to add 227 1/4 square feet to its facilities in the spring of 1965.

Our growth in net assets from $105,100 (there's no prize for guessing who put in the $100) on May 5, 1956 when the first predecessor limited partnership.(Buffett Associates, Ltd. ) was organized, to $26,074,000 on 1/1/65 creates the need for an occasional reorganization in internal routine. Therefore, roughly contemporaneously with the bold move from 682 to 909 ¼ square feet, a highly capable is going to join our organization with responsibility for the administrative (and certain other) functions. This move will particularly serve to free up more of Bill Scott's time for security analysis which is his forte. I’ll have more to report on this in the midyear letter.

Bill (who continues to do a terrific job) and his wife have an investment in the Partnership of $298,749, a very large majority of their net worth. Our new associate (his name is being withheld until his present employer has replaced him), along with his wife and children, has made an important investment in the Partnership. Susie and I presently have an interest of $3,406,700 in BPL which represents virtually our entire net worth, with the exception of our continued holding of Mid-Continent Tab Card Co., a local company into which I bought in 1960 when it had less than 10 stockholders. Additionally, my relatives, consisting of three children, mother , two sisters, two brothers-in-law, father-in-Law, four aunts, four cousins and six nieces and nephews, have interests in BPL, directly or indirectly, totaling $1,942,592. So we all continue to eat home cooking.

We continue to represent the ultimate in seasonal businesses --open one day a year. This creates real problems in keeping the paper flowing smoothly, but Beth and Donna continue to do an outstanding job of coping with this and other problems.

Peat, Marwick, Mitchell has distinguished itself in its usual vital role of finding out what belongs to whom. We continue to throw impossible deadlines at them --and they continue to perform magnificently. You will note in their certificate this year that they have implemented the new procedure whereby they now pounce on us unannounced twice a year in addition to the regular yearend effort.

Finally -and most sincerely -let me thank you partners who cooperate magnificently in getting things to us promptly and properly and thereby maximize the time we can spend working where we should be -by the cash register. I am extremely fortunate in being able to spend the great majority of my time thinking about where our money should be invested, rather than getting bogged down in the minutiae that seems to overwhelm so many business entities. We have an organizational structure which makes this efficiency a possibility, and more importantly, we have a group of partners that make it a reality. For this, I am most appreciative and we are all wealthier.

Our past policy has been to admit close relatives of present partners without a minimum capital limitation. This year a flood of children, grandchildren, etc., appeared which called this policy into question; therefore, I have decided to institute a $25,000 minimum on interests of immediate relatives of present partners.

Within the coming two weeks you will receive:

(1) A tax letter giving you all BPL information needed for your 1964 federal income tax return. This letter is the only item that counts for tax purposes.

(2) An audit from Peat, Marwick, Mitchell & Co. for 1964, setting forth the operations and financial position of BPL as well as your own capital account.

(3) A letter signed by me setting forth the status of your BPL interest on 111165. This is identical with the figure developed in the audit.

(4) Schedule “A” to the partnership agreement listing all partners.

Let Bill or me know if anything needs clarifying. Even with our splendid staff our growth means there is more chance of missing letters, overlooked instructions, a name skipped over, a figure transposition, etc., so speak up if you have any question at all that we might have erred. My next letter will be about July 15th" summarizing the first half of this year.

Cordially,

Warren E. Buffett