问题索引

洛杉矶1992VS香港2019?《编辑部的故事》类似未能涌现的原因?证监会的在证券市场的作用?好公司的标准?垄断公司一定好?折现现金流模型中折现率和折现年限的选择?

既然员工退休金要认列负债,那么认股权证是否也应该认列?认股权证进入损益表的难点?

资料来源:

·大象点映《激荡四十年》

·《追寻价值之路 - 1990~2020中国股市行情复盘》

·《芒格之道 - 查理·芒格股东会讲话》

·BERKSHIRE HATHAWAY INC. - 《SHAREHOLDER LETTERS》

·喜诗勘地 - 雪球 - 伯克希尔-哈撒韦编年史

关键词:劳合社 S&P500 好公司的标准 如何发掘好公司 航空业 退休金负债 认股权证的公司成本

查理·芒格

机会与等待(去年一样的)

“我们目前几乎没承接什么保险业务。行业的价格太低了,我们不愿意做。西科、互助储蓄、伯克希尔•哈撒韦有一个共同点:如果我们不喜欢别人做的事,我们就不跟着做。至少我们过去始终如此,但我不保证,我们将来能仍然如此。大多数人,看到竞争对手都朝着一个方向跑,自己在那傻站着,就受不了了,明知大家跑的方向是错的,也还是跟着跑。这种行为有着深层次的心理学原因。”

“我们持有大量资金,却找不到条件合适的保险业务。只要条件合适,我们愿意在保险业务中投人几千万、几亿美元。现在很难找到合适的保险业务,除非是经历了几十年的积淀,建立了一套独一无二的模式。例如,州立农业保险、盖可保险 (GEICO),这两家公司都有自己独特的模式。它们的生意模式好、管理水平高,而且有几十年的历史。像它们这样的公司,不愁没有新业务。特别是要抓住确定性高的(认知范围内的)大机会,不可能对所有机会都看透。”

银行业普遍激励与报酬不对应(前年一样的)

“劳合社已经很了不起了。虽然制度早已存在漏洞,它竟然能坚持这么多年,到现在才爆发问题。这说明劳合社确实具有深厚的底殖,英国的文明确实有很强的生命力。

银行业存在同样的问题。银行按照发放货款的规模给员工提成,至可七八年后货款能否收回,都不影响员工的薪水。这也是一种存在漏洞的街度,可能导致严重的问题。”

沃伦·巴菲特

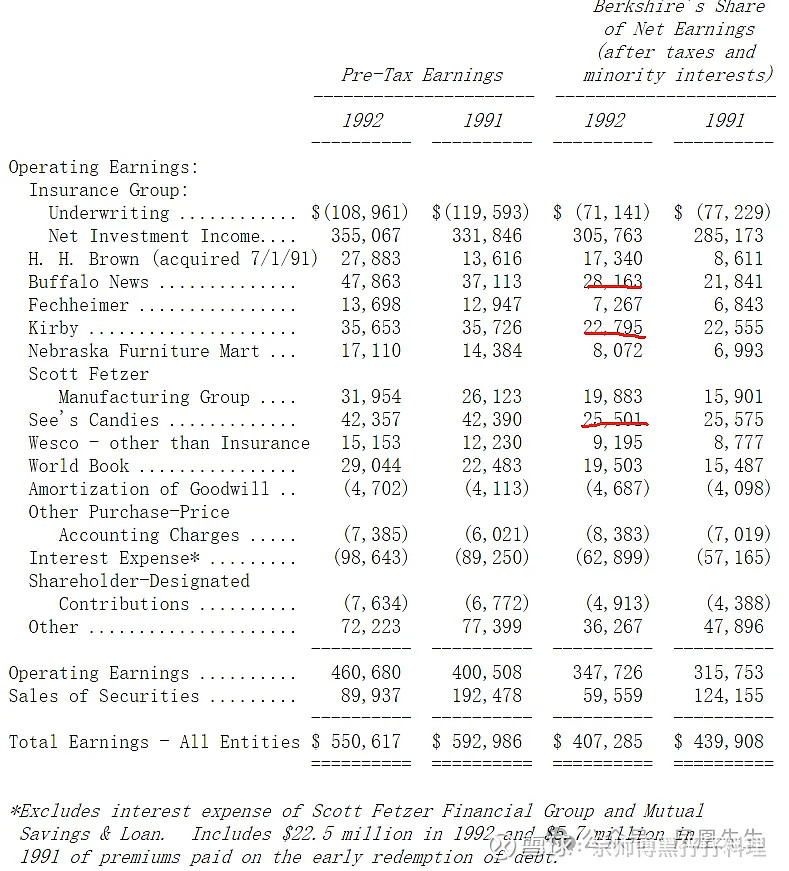

当年各事业盈余来源非保险类前三:

1.Buffalo News. 《布法罗新闻》

2.See's Candies 喜诗糖果

3.Kirby 真空吸尘器品牌,Scott Fetzer的一个部门,后者是伯克希尔在1986年收购

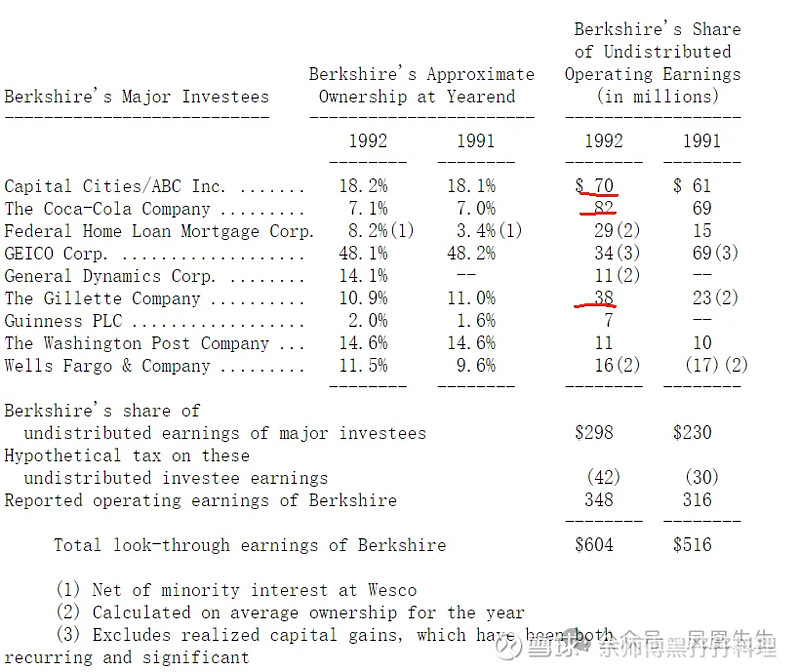

当年投资收益前三(Berkshire's share of undistributed earnings of major investees):

1.The Coca-Cola Co. 可口可乐

2.Capital Cities/ABC Inc.大都会通信公司/美国广播公司

3.Gillette 吉列

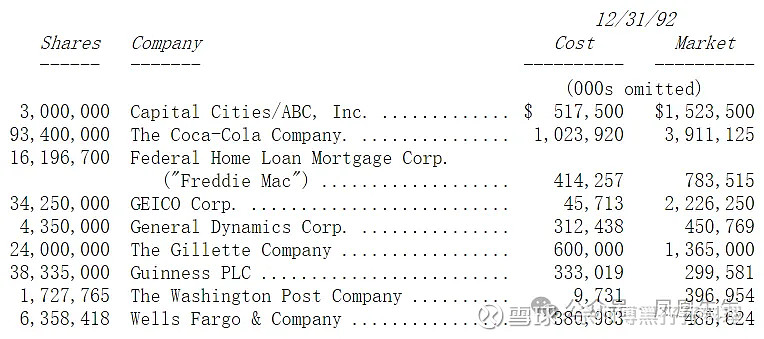

当年持股市值前三:

1.The Coca-Cola Co. 可口可乐

2.GEICO Corp. 盖可保险

3.Capital Cities/ABC Inc.大都会通信公司/美国广播公司

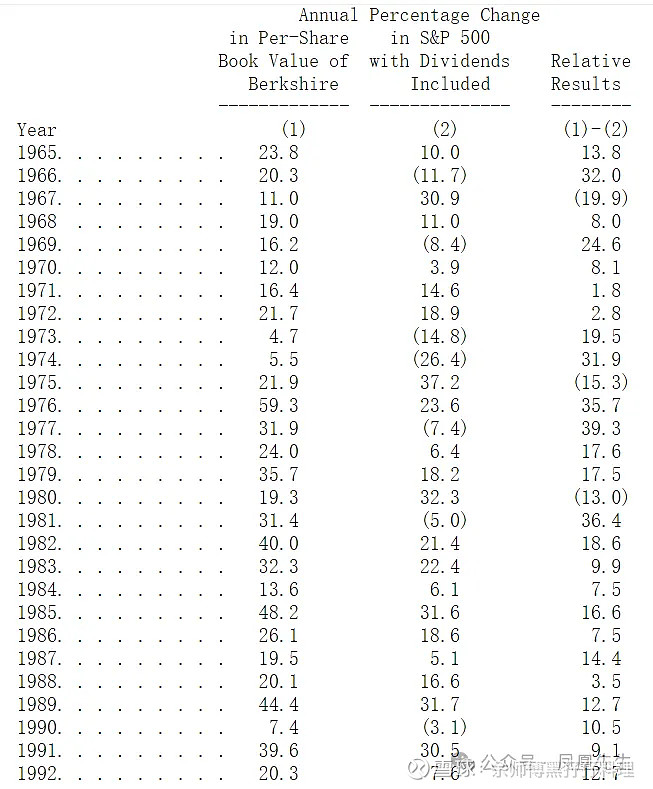

S&P500的比较

当年开始,在年报的首页放置每年公司净值变化与标普500指数(含现金股利)变化的比较。

在对比时,需要考虑三点,一是早期纺织业务占比大,直至最近才增加其他投资,比较才有意义,二是税负不一样,投资证券所产生的收益与资本利得必须要负担相当重的税负,举例投资利得税前有18%税后就会只有13%(both the income and capital gains from our securities are burdened by a substantial corporate tax liability whereas the S&P returns are pre-tax),三是对未来预测能跑赢标普500。

虽然,股市短期预测意义不大(hort-term market forecasts are poison and should be kept locked up in a safe place, away from children and also from grown-ups who behave in the market like children),但长期,还是称重器(stocks cannot forever overperform their underlying businesses),如果短期是投票器。这是巴芒对未来有信心的底气。

有能力,迟早打出全垒打(In baseball lingo, our performance yardstick is slugging percentage, not batting average)。

看数据,已经连续近30年正收益,连续10年跑赢标普500。

购买

职业经理人,买企业/买业务,有时会有些随意/童话化(以王子的价格去买青蛙,以为一吻就能成王子……many acquisition-hungry managers were apparently mesmerized by their childhood reading of the story about the frog-kissing princess. Remembering her success, they pay dearly for the right to kiss corporate toads, expecting wondrous transfigurations),因为成本/学费是股东交的(the CEO receives the education but the stockholders pay the tuition)。

甚至,一次失败并不会阻止新的尝试( Initially, disappointing results only deepen their desire to round up new toads)。

在巴菲特眼中,本来便宜是第一位的,结果并不理想(毕竟便宜可能没好东西,但好在便宜,用青蛙的价格买了青蛙……dated a few toads. They were cheap dates……),好在认识到了错误,就像高尔夫选手““不断的练习无法达到完美的境界,只会让错误巩固”( "Practice doesn't make perfect; practice makes permanent." )。

所以开始试着以合理的价格买进好公司(I revised my strategy and tried to buy good businesses at fair prices rather than fair businesses at good prices)。

好公司

去年谈了好业务的三个标准(需求明确,难以或没有替代品,不受价格上的管制)

今年谈了投资对象(好公司)的四个标准:

可以理解把握的that we can understand;

有长期发展前景with favorable long-term prospects;

经营者才德兼具operated by honest and competent people;

合理价格available at a very attractive price.

里面,关于估值是最难的。

也是最难的。

在估量价格是否合理时,价值派和成长派("value" and "growth" ),是主流的观点和争论。

价值派常用低PE、低PB、高股息率等作为指标,但及时一个股票同时符合这三者样,也不一定价值低于价格(Unfortunately, such characteristics, even if they appear in combination, are far from determinative as to whether an investor is indeed buying something for what it is worth and is therefore truly operating on the principle of obtaining value in his investments),也不一定属于价值投资( "value investing")。

成长,确实对企业价格有利。

但前提是,企业把资金的投入可以产生增量收益(incremental returns),可以产生净价值(only when each dollar used to finance the growth creates over a dollar of long-term market value)。如果,成长只是资产额上升,ROE下降,甚至净利润下降,就没有意义了。

毕竟资产/股票的价格,就是未来利润/收益的折现(John Burr Williams…… The value of any stock, bond or business today is determined by the cash inflows and outflows - discounted at an appropriate interest rate - that can be expected to occur during the remaining life of the asset)。

后来在1995年的股东会上,就有人问巴菲特会用多少年来折现。

巴菲特认为,折现现金流的估值方法很重要,但具体的折现率和折现年限并不重要(所以,也可以认为,需要精确计算的投资不是好投资)。

抛开价格,投资者都希望投未来现金流多的企业,也即希望投资那种在一段长时间内,可以将大笔的资金运用在高报酬的投资上的企业(the best business to own is one that over an extended period can employ large amounts of incremental capital at very high rates of return. )。

但估计未来,谈何容易(an analyst - even one who is experienced and intelligent - can easily go wrong in estimating future "coupons" )。

最终,结论有落在了能力圈和安全边际(margin of safety)两个关键词上。

能力圈,是为了理解商业模式后能预测现金流(If a business is complex or subject to constant change, we're not smart enough to predict future cash flows),做得少错的少,在认知范围内操作就不会犯大错误( An investor needs to do very few things right as long as he or she avoids big mistakes)。

安全边际,如果预测的折现价格与股票价格相近,那没必要购买,因为没有安全边际。

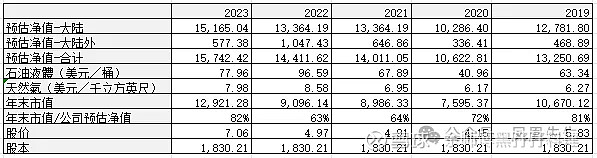

中国石油是有每年公开自己公司的预估净值(未来现金流折现值)。

航空业

竞争激烈(I knew the industry would be ruggedly competitive, but I did not expect its leaders to engage in pro longed kamikaze behavior,pro longed kamikaze-神风特别攻击队-かみかぜとくべつこうげきたい,在第二次世界大战末期日本为了抵御美国军队强大的优势,利用日本人的武士道精神,按照“一人、一机、一弹换一舰”的要求,对美国舰艇编队、登陆部队及固定的集群目标实施的自杀式袭击的特别攻击队。)

工会压力(Capitulating to the striking union, however, would have been equally disastrous: The company was burdened with wage costs and work rules that were considerably more onerous than those encumbering its major competitors, and it was clear that over timeany high-cost producer faced extinction)

管理要求(requires far more managerial skill than does a business with fine economics.Unfortunately, though, the near-term reward for skill in the airline business is simply survival, not prosperity)

当时巴菲特选中的全美航空(USAir)的优先股,全美航空在2013年与美国航空(NASDAQ:AAL)合并,目前美国航空市值仅93亿美元,每股净资产-8.38,更奇葩的波音(NYSE:BA),每股净资产-27.73,市值有1084亿。

会计准则Accounting

两项已经实行的准则。

一个关于未实现收益(unrealized appreciation)的递延所得税(deferred taxes)税率。

一个是需要认列员工退休金负债(recognize their present-value liability for post-retirement health benefits),这个也很合理,毕竟这是公司的偿债压力。轻的,如果不确认负债,就会使净值偏高(后来,也见有讨论,因为员工数辞退的高成本,是否也应该列入公司的预计负债),重的可能威胁企业生存(In health-care, open-ended promises have created open-ended liabilities that in a few cases loom so large as to threaten the global competitiveness of major American industries)。

巴菲特,在1982年,就曾差点买下一家有沉重退休金负债的公司,当时是因为其他原因被其他买家收入,但这家公司没多久就关门了。

所以,认清本质很重要,是腿还是尾巴,光说不算(one of Abraham Lincoln's favorite riddles: "How many legs does a dog have if you call his tail a leg?" The answer: "Four, because calling a tail a leg does not make it a leg." )。

巴菲特认为有一样东西也应该认列成本费用,进入损益表,但一直没有执行——

认股权证(stock options)。

有人认为选择权不好定价(hard to value),有人认为公司没掏钱( options should not be viewed as a cost because they "aren't dollars out of a company's coffers." ),有时, 行权价格也会高于现在价格(使得当前没有价值,"out-of-the-money" options ,hose with an exercise price equal to or above the current market price)。但,只要不进入损益表,就使得股东权益摊薄了,账面盈利虚高了。

实际上,只要股权是有价值的,那么认股权证也有价值(that companies incur costs when they deliver something of value to another party and not just when cash changes hands)。

既然,CEO/管理层乐意接受认股权证作为报酬,报酬就是公司应该认列到损益表的费用。