赛斯克拉曼(Seth Klarman)的Baupost集团是世界第十一大对冲基金。在“史上最伟大的基金经理”名单上,克拉曼排名第四。塞思·克拉曼也是一个著名的价值投资作家,他写的著作《安全边际》一度被炒到1500美元一本。克莱曼毕业于哈佛商学院,当时他在哈佛商学院的教授比尔·比尔夫(Bill Poorvu)要求克拉曼帮忙理财。比尔夫和他的合作伙伴——霍华德史蒂文生(Howard Stevenson)、约旦·巴鲁克(Jordan Baruch)、艾萨克·奥尔巴赫(Isaac Auerbach)用他们的名字合并创建了Baupost公司,克拉曼的名字不包括在内。但有趣的是,当他们聘请克拉曼时,他们也并不想将基金的名称改为Baupostkl。

人物简介

赛斯克拉曼(Seth Klarman)是投资合伙集团Baupost的价值投资者和投资组合经理。Baupost集团成立于1983年,现管理规模70亿美元,自成立以来每年年均回报率达到近20%。克拉曼在美国康奈尔大学获得了经济学学士学位,后来在哈佛大学获得MBA学位。

投资理念

克拉曼投资广泛,从传统的价值股票到多样化的投资产品,例如不良债务、清算、外国股票或债券。其掌管的Baupost Group投资横跨股票、债券和房地产等不同的资产类别,年均复合回报率达到16.4%,累计为投资人带来了226亿美元的收益。当投资机会很少时,克拉曼不介意“什么事都不干”,持有现金,作为旁观者的想法完全不受干扰。事实上,在2005年和2006年,其近一半的投资组合是以现金形式持有的。他警告投资者说,投资不仅仅是产生绝对的回报值,投资者大多时候只专注于“回报率”这个数字,却往往忽略产生了这个数字所带来的风险。

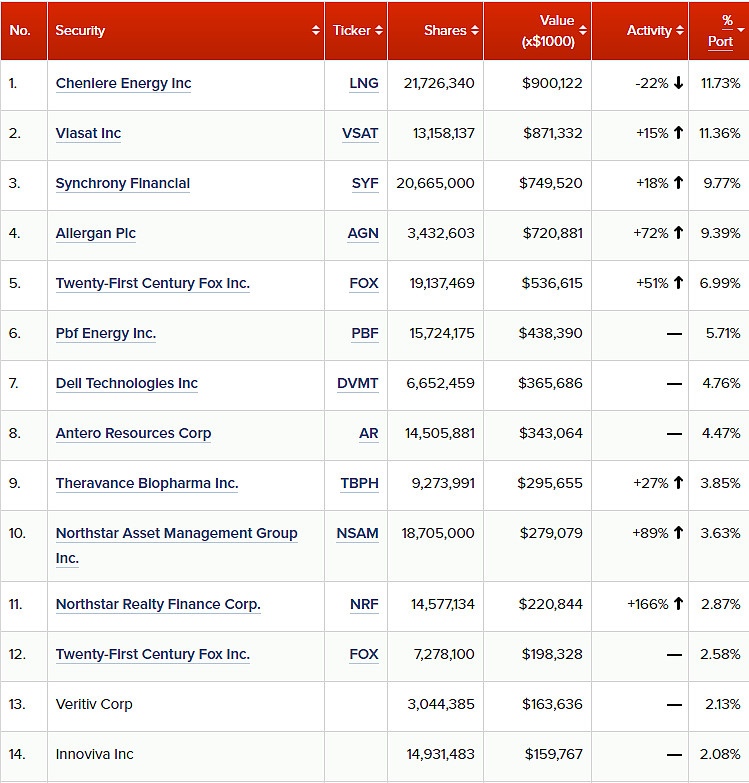

仓位一览图

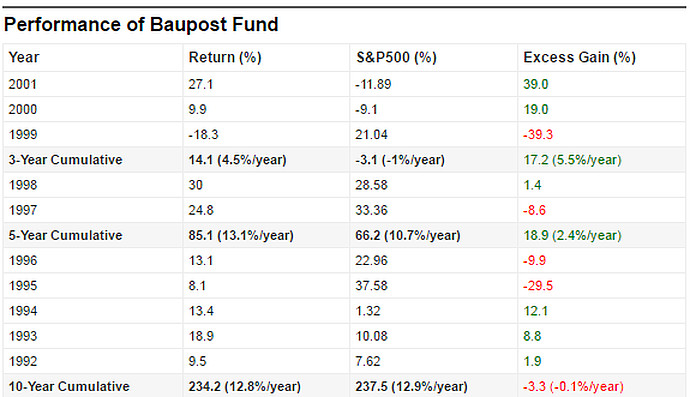

关于Baupost基金历史表现

大佬谈股

赛斯克拉曼:怎么寻找“打折股”?

克拉曼的投资风格很简单——寻找市场价比内在价值低的公司。这看似简单,做起来却并不简单。 克拉曼特殊的价值投资风格不仅限于只是估测某个公司在未来几年内的增长,相反克拉曼把精力放在现有市场价值远低于资产价值的公司。通常情况下,试图找到这些公司需要大量的工作和精力,这使投资者失望。

通过观察克拉曼的投资组合,我们得知,世界上一些有名的价值投资者都害怕跟随他的投资方式。以Viasat Inc.(NASDAQ:VSAT) 为例,在由GuruFocus跟踪的许多大佬的投资组合中,克拉曼是少数持有卫星供应商股份的四个投资者之一。 PBF Energy Inc.(NYSE:PBF) 是克拉曼喜欢的另一个股票,但华尔街的其他人似乎表示不看好这只股票。

为了帮助您了解克拉曼为什么喜欢这些股票,以及他的投资策略给您提供一些启示,我们收集了这位伟大的投资者多年来在各种书籍、采访和投资者信件中发表的言论。

“Things that have never happened before are bound to occur with some regularity. You must always be prepared for the unexpected, including sudden, sharp downward swings in markets and the economy. Whatever adverse scenario you can contemplate, reality can be far worse.”

“以前从来没有发生过的事情一定会发生的规律。您必须永远为意想不到的事情做好准备,包括市场和经济突然大幅下滑。无论你考虑怎样不利的情况,现实情况可能会糟糕得多。

“You must buy on the way down. There is far more volume on the way down than on the way back up, and far less competition among buyers. It is almost always better to be too early than too late, but you must be prepared for price markdowns on what you buy.”

“你一定要买下去。在股票价格下降的路上还有更多的交易量,而且买家的竞争也要小得多。买早永远比买晚好,但是你必须做好心理准备对您购买的商品进行降价销售。”

“The latest trade of a security creates a dangerous illusion that its market price approximates its true value. This mirage is especially dangerous during periods of market exuberance. The concept of 'private market value' as an anchor to the proper valuation of a business can also be greatly skewed during ebullient times and should always be considered with a healthy degree of skepticism.”

“股票的最新交易容易给投资者造成一个危险的错觉——其市场价格接近其真实价值。这种想法在市场繁荣期间特别危险。“私有市场价值”作为企业估值的一个主要观念,也可能在市场繁盛的时期受到极大的偏见,投资者应该保持警惕,以正常的怀疑态度来考量市场。”

“Beware leverage in all its forms. Borrowers – individual, corporate or government – should always match fund their liabilities against the duration of their assets. Borrowers must always remember that capital markets can be extremely fickle, and that it is never safe to assume a maturing loan can be rolled over. Even if you are unleveraged, the leverage employed by others can drive dramatic price and valuation swings; sudden unavailability of leverage in the economy may trigger an economic downturn.”

“小心任何形式的杠杆。借款人不论是个人、公司或政府——我们应始终将资产负债与其资产使用期限相匹配。借款人必须永远记住,资本市场可能非常脆弱,单纯认为成熟的贷款可以运转,这种想法是永远不安全的。即使你是无杠杆的,其他人所采用的杠杆作用也会带来巨大的价格和估值波动;经济突然的杠杆作用可能引发经济衰退。”

“Risk is not inherent in an investment; it is always relative to the price paid. Uncertainty is not the same as risk. Indeed, when great uncertainty – such as in the fall of 2008 – drives securities prices to especially low levels, they often become less risky investments.”

“投资风险不是固有的,它与支付的价格是相对的。不确定因素与风险不一样。例如像2008年秋季这样的巨大的不确定因素,使得证券价格达到前所未有的低价,而此时往往意味着小风险。”

“Attention to risk must be a 24/7/365 obsession, with people – not computers – assessing and reassessing the risk environment in real time. Despite the predilection of some analysts to model the financial markets using sophisticated mathematics, the markets are governed by behavioral science, not physical science.”

“注意风险必须是一年365天24小时的事情,人不是计算机,没有办法实时评估和重新评估风险环境。尽管一些分析师倾向于使用复杂的数学模型来模拟金融市场,但市场应该用行为科学来衡量,而不是物理科学来管理。”@今日话题 @庐州闲人 @肖磊看市 @若无其事 @黄但斌 @Mario @钟正生 @韩韩超 @价值at风险 @陈小邪美股投资 @Mario @东兴证券林阳